Charles Schwab manages 38.9 million active brokerage accounts and holds $12.22 trillion in client assets. For years, investors in these accounts have been able to access Bitcoin and Ethereum through ETFs, crypto-related stocks, and futures contracts.

A gradual launch from the second quarter closes the gap with direct investments. Schwab Crypto, offered by Charles Schwab Premier Bank, SSB, will allow eligible customers to directly buy and sell Bitcoin and Ethereum.

The offer is available in all US states except New York and Louisiana, on a schedule that starts with employees and a small initial cohort before expanding.

Why it’s important: Schwab does not introduce crypto to a crypto-native audience. It tests whether direct ownership of Bitcoin and Ethereum can fit into a traditional brokerage client’s workflow. If this model gains traction, the implications will extend beyond Schwab to product design, broker-dealer competition, and the next layer of retail crypto adoption.

The product architecture includes a structural boundary that customers and operators will immediately feel. Schwab Crypto operates through a dedicated account with an affiliated banking subsidiary.

This means that the structure is in a separate account from the brokerage accounts where investors already hold stocks, bonds and ETFs. Crypto assets do not carry any SIPC or FDIC protection.

Schwab does not currently accept crypto deposits and does not settle crypto securities or futures transactions. General public access is real and it happens under conditions carefully controlled and defined by brokers.

What motivated the choice of the calendar until 2026 was a political calendar that dissolved three major institutional frictions in four months.

In January 2025, SAB 122 repealed previous SAB 121 crypto protection guidelines that had made the custodial economics unattractive to traditional banks.

In March 2025, the OCC reaffirmed that cryptocurrency custody, certain stablecoin activities, and participation in distributed ledgers are permitted for domestic banks and removed the no-objection supervisory requirement.

In April 2025, the Federal Reserve withdrew its previous crypto guidelines and decided to supervise these activities through the standard process.

Schwab CEO Rick Wurster described these regulatory measures as “green enough” for large companies to expand into crypto, and the timing of the launch confirms how much the political calendar has directly shaped the product timeline.

| Date | Regulatory/market development | Why it mattered to Schwab |

|---|---|---|

| January 2025 | SAB 122 canceled SAB 121 | Reducing a key accounting friction around crypto custody |

| March 2025 | OCC stated that crypto custody, certain stablecoin activities and participation in DLT are permitted; removal of no-objection requirement for surveillance | Bank-Related Crypto Business Just Got Easier to Pursue |

| April 2025 | The Federal Reserve withdrew its previous crypto guidelines and moved to normal supervision | Reduced friction from special processes for large institutions |

| March 2026 | Schwab Research Says Bitcoin Has Become a Mainstream Asset | Showed that internal positioning had evolved towards standardization |

| Q2 2026 | Schwab began phased crypto rollout | Product timing followed policy change |

The asset that Schwab normalizes

In March 2026, Schwab published a study describing Bitcoin as having become a mainstream asset and noting that by some measures it had become less volatile than some stocks in the Magnificent 7.

The research reflects the internal positioning that led to direct trading as a natural next step.

Reuters reported Wurster’s view that the target user is an investor who already owns stocks and bonds and wants to hold a small share of Bitcoin or Ethereum alongside those positions.

This is a narrower, more defensible market than the speculative base that drove 2021 volumes. Schwab is creating a product for the traditional investor who already trusts the brokerage brand and wants direct exposure within the brokerage environment they use.

Schwab is entering a market that Fidelity already occupies. Fidelity’s Crypto Account allows customers to buy, sell and transfer crypto through its platform and the Fidelity app alongside their existing brokerage positions.

E*TRADE has released a page for direct trading of Bitcoin, Ethereum and Solana soon, and reports indicate that Morgan Stanley plans to run this service through Zerohash in the first half of 2026.

Schwab enters this race as a standard-setter of scale, being the company whose distribution footprint turns a multi-broker model into an industry default.

When Fidelity launched direct crypto, the market could read it as the idiosyncratic appeal of a company.

When Schwab, Fidelity and E*TRADE each offer a direct access version of BTC and ETH, the mental category moves. When Schwab, Fidelity, and E*TRADE each offer some form of direct access to BTC and ETH, direct crypto ownership sits on the same mental shelf as any other optional asset wrapper in a diversified brokerage account.

Schwab’s own site already markets crypto exposure “from a brand you know,” and the launch extends that brand promise from the packaging to the asset itself.

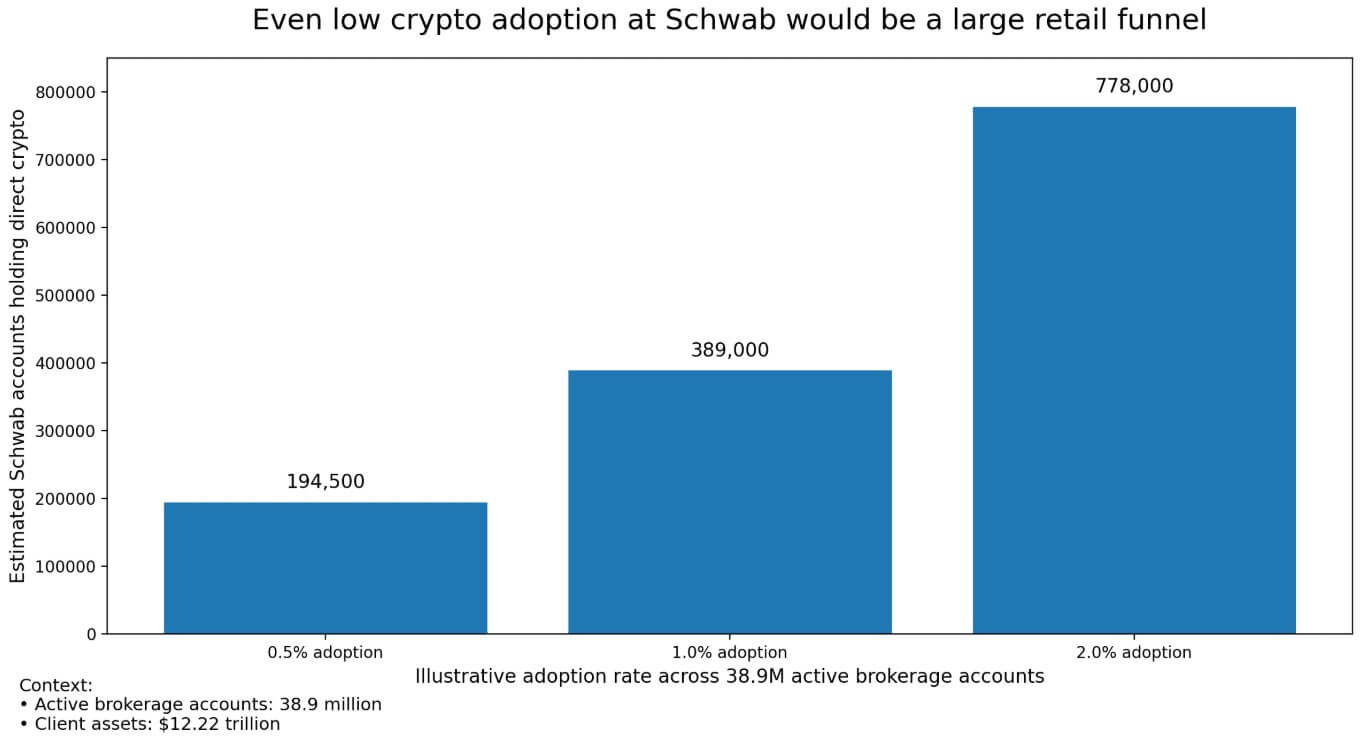

A distribution thought experiment frames scale without making too many claims for price increases.

If 0.5% of Schwab’s 38.9 million accounts ultimately hold direct cryptocurrencies, that equates to approximately 194,500 accounts. At 1% this becomes around 389,000, and at 2% adoption this funnel reaches around 778,000 accounts.

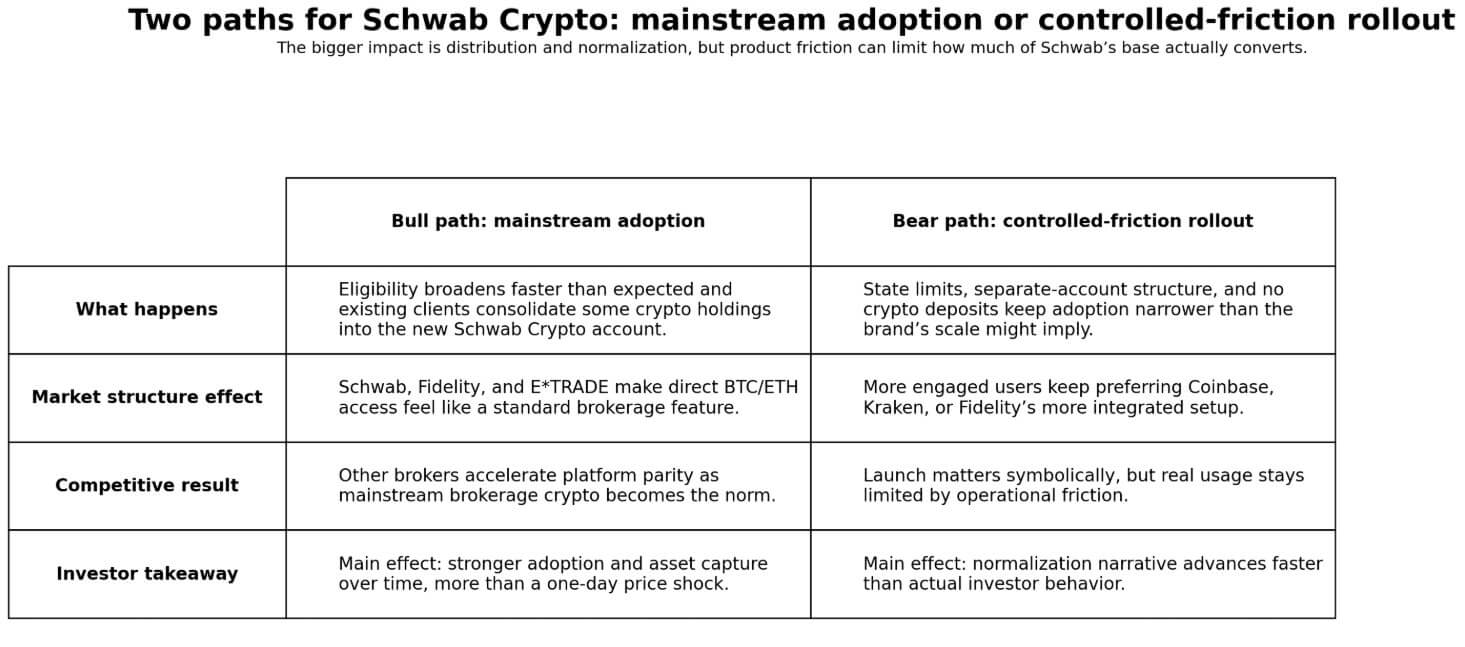

Two ways from here

The bullish path opens if Schwab expands eligibility faster than the progressive language suggests, and if the product experience proves clear enough for existing customers to consolidate their crypto holdings into the new account.

In this scenario, Fidelity, E*TRADE and Schwab together create a demand flywheel within the traditional brokerage channel, the type of end-investor adoption that Citi cited in its bullish pitch of $165,000 for Bitcoin and $4,488 for Ethereum.

Schwab’s distribution footprint alone would push any brokers that still route their crypto clients exclusively to ETFs or educational pages to accelerate their own platform parity timelines.

The bear’s path is through friction. The Schwab Crypto Account’s state restrictions, bank branch architecture, lack of crypto deposits, and current transfer limitations each create shortcomings compared to crypto sites that more engaged users will notice.

If this friction limits adoption and investors who want direct exposure to crypto continue to prefer the more integrated setup of Coinbase, Kraken or Fidelity, the launch reads as operationally thin.

An investor who wants crypto to sit alongside stocks in a single operational view may find in the banking subsidiary an exposure vehicle with stricter product limits than the brand’s integrated portfolio framing implies.

The next readable data point comes when Schwab reveals how quickly the initial Q2 cohort is converting and whether the broader rollout is accelerating on schedule.

How quickly Schwab moves this cohort to general availability will indicate to the market whether this launch is a truly large-scale ambition or a carefully managed compliance exercise.