The total stablecoin supply hit a record high of $315 billion in the first quarter of 2026, up about $8 billion quarter-over-quarter, even as the broader crypto market contracted.

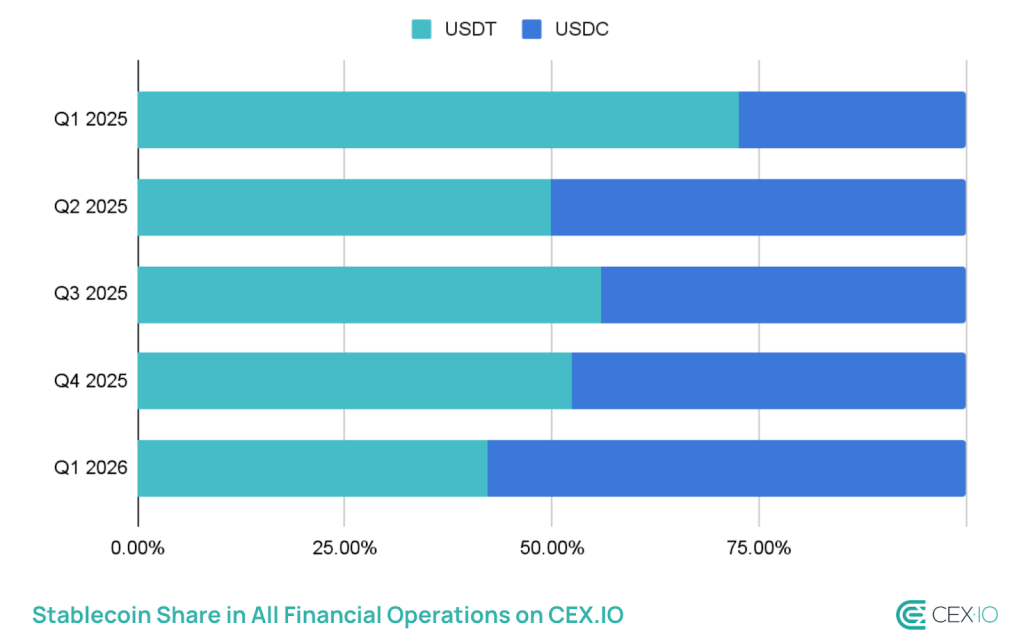

The headline number masks a clearer story underneath: USDC is gaining ground relative to USDT, and the gap is closing faster than most market participants expected.

USDC supply has surged 220% since late 2023 to approximately $78 billion, driven by B2B institutional settlement, payroll infrastructure, and programmatic payment rails built by Visa and Stripe.

USDT, which remains the dominant issuer in terms of commodity supply, saw its stock fall – a divergence reported by CEX.IO as one of the defining market dynamics of the quarter.

- The total supply of stablecoins hit a record $315 billion in the first quarter of 2026, up about $8 billion quarter-over-quarter – the slowest growth since the fourth quarter of 2023, but still expanding during a market contraction.

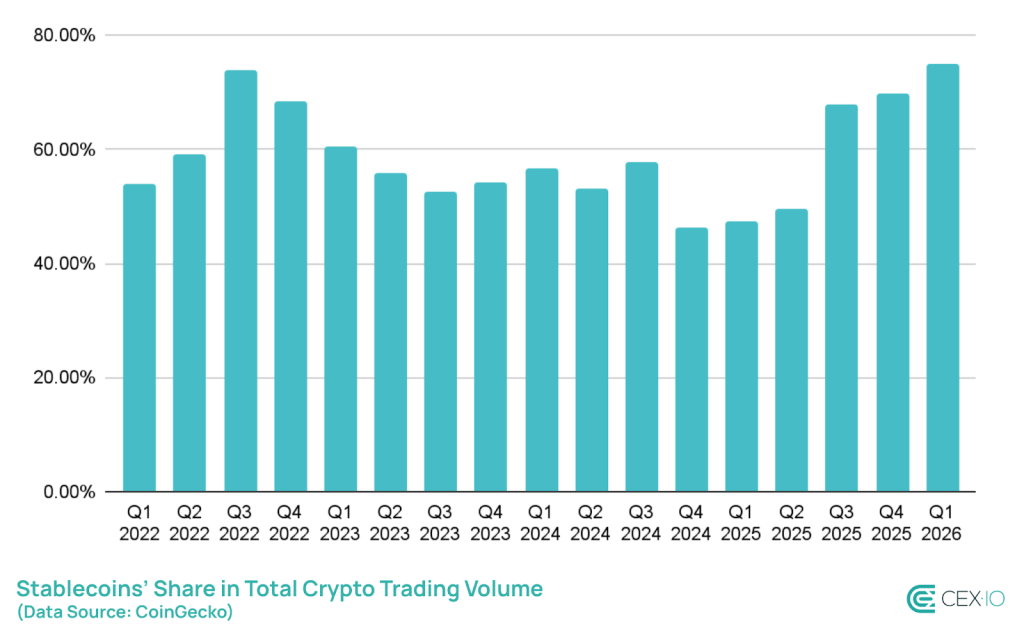

- Stablecoins accounted for 75% of total crypto trading volume in the first quarter – the highest share on record.

- Total stablecoin trading volume has exceeded $28 trillion, surpassing Visa and Mastercard combined.

- USDC supply has surged 220% since late 2023 to around $78 billion; USDT market share fell amid the divergence.

- Retail transfers fell 16% – the steepest decline on record – while bots generated around 76% of all stablecoin trading volume.

- Yielding stablecoins are now a $3.7 billion subsector, introducing new risks of fragmentation and regulation.

Discover: The best crypto to diversify your portfolio during market turbulence

Stablecoins also captured 75% of total crypto trading volume in the first quarter – the highest share ever – while total trading volume surpassed $28 trillion, a figure that now regularly exceeds that of major payment networks like Visa and Mastercard combined. The slowdown in the growth rate is real; demand does not evaporate.

USDC’s gain is a regulation story, not just a market share story

The rise of USDC is not an adoption of organic retail. CEX.IO data indicates that institutional programmatic money – B2B corridors, salary settlement, cash management, is the main driver.

USDC transaction speed reached 90x with an average transfer amount of $557, a profile consistent with frequent, smaller institutional transactions rather than whale movements.

Circle’s positioning ahead of potential US stablecoin legislation was deliberate. With the Clarity for Payment Stablecoins Act still under debate and regulatory frameworks for digital assets evolving in Washington, regulated issuers like Circle have a structural advantage in onboarding compliance-sensitive institutional capital. This distinction is important: it is not just about market share gained on the basis of yield or depth of liquidity.

Analysts reviewing the quarter described this shift bluntly: “This is not retail adoption; this is institutional programmatic money. » The figure confirms that this is the average USDC transfer size of $557 – dwarfed in absolute terms by USDT’s larger individual transactions, but indicative of high-frequency automated institutional flows that reflect broader tokenization and institutional adoption trends reshaping digital asset infrastructure.

If US stablecoin legislation is passed with provisions favoring regulated and audited issuers, USDC’s gain will become structural. If this stops, the competitive advantage narrows and USDT’s entrenched liquidity depth reasserts its dominance.

USDT still leads, but competitive gap narrows

USDT remains the largest stablecoin in terms of supply and the dominant liquidity instrument in emerging market corridors and Tron-based DeFi.

Its focus on Tron, where low fees drive retail and cross-border transfer volume, gives it a user base that USDC’s Ethereum-centric institutional footprint does not directly compete with. Again.

The drop in USDT’s market share in the first quarter comes with the largest decline on record in retail transfers – down 16% – which reduces one of USDT’s main use cases.

Simultaneously, bots now account for approximately 76% of total stablecoin trading volume, meaning the organic retail demand that historically anchored USDT’s dominance in high-frequency, low-value transfers is contracting.

CEX.IO reported this as evidence of a “more sophisticated, but potentially less organic, market structure.”

Tether’s response has been limited to quarterly reserve certifications and geographic expansion rather than product-level innovation. This is a defensible position even if it leads to network effects.

This becomes a liability if institutional capital flows continue to transform into regulated instruments and programmatic USDC integrations deepen into Western payments infrastructure.

Watch Circle’s May statement and Tether’s Q2 report to see if the supply divergence is widening. If USDC rises above $90 billion while USDT stagnates, this quarter’s move in stocks will stop looking like an incident and start looking like a trend.

The total supply figure of $315 billion tells you that stablecoins are the supporting layer of the market. The USDC/USDT breakdown tells you who is building on it.

Explore: Best Pre-Launch Token Sales with Asymmetric Upside Potential

Post-Stablecoin Crypto Supply Hits $315 Billion in Q1 as USDC Gains, USDT Slips First on Cryptonews.