Get news delivered straight to your inbox. Subscribe to the Empire newsletter.

Stablecoins are clearly having a moment of popularity.

While the rest of cryptocurrencies have been moving sideways, the market cap of stablecoins has been steadily increasing. It now stands at $170 million, according to rwa.xzy, although there has been a slight decline in recent days.

Castle Island Ventures, in collaboration with Artemis, Visa and Brevan Howard Digital, has conducted a new study that examines the prevalence of stablecoins in selected emerging markets. The survey covered approximately 2,500 cryptocurrency users in Nigeria, India, Turkey, Indonesia and Brazil.

“Our survey results contradict the common belief that stablecoins are used exclusively as a tool for speculative trading of crypto assets. Forty-seven percent of surveyed crypto users cite dollar savings as the purpose of their stablecoin, 43% cited efficient currency conversion, and 39% stated yield generation. Access to cryptocurrency exchanges remains the primary use case for respondents, but a long tail or ordinary (non-crypto) economic activities are also evident,” the report states.

Learn more: Stablecoins are ‘a better product’ than local currencies in emerging economies, says Carrica

“The results are clear: non-cryptocurrency uses represent a significant share of stablecoin usage patterns in the countries studied.”

Nic Carter of Castle Island Ventures told Blockworks he was curious to track the data because he wanted to better understand how people are using stablecoins.

From there, Carter will present his findings in Washington DC. Lawmakers on Capitol Hill and various US officials have been quite vocal about their views on stablecoins. Senators Kirsten Gillibrand and Cynthia Lummis are also pushing for regulation around stablecoins.

“If you look at emerging markets, it’s a case of currency substitution where savings would be held in naira, Turkish lira or Indian rupee, and it’s actually converted into dollars,” Carter explained.

“So this is positive buying pressure for the dollar and all dollar assets held by stablecoin issuers (which are Treasuries). What I mean is there is a flow into the dollar. This is a new source of demand. This is very significant and it obviously supports US interests.”

But while that may impress U.S. lawmakers, some of the results may not be to the liking of those in Nigeria, for example. As we’ve reported before, Nigeria became more hostile toward cryptocurrencies earlier this year, arresting two Binance executives (American Tigran Gambaryan remains in custody in the country) and accusing Binance of tax evasion and money laundering.

Nigeria’s attempts to regulate the sector may not have been as successful as the country had hoped, according to data from the report. The investigation took place from May to June earlier this year, with some data on the channel collected through July. Nigeria arrested Gambaryan in late February.

“Nigerians love stablecoins,” Carter noted. The country may even have a right to be “paranoid,” given that the full survey results show Nigeria came out on top in every category.

Users in the country “conduct the most transactions, stablecoins make up the largest share of respondents’ wallets, they report the largest share of non-cryptocurrency trading uses for stablecoins, and they maintain the highest self-reported knowledge of stablecoins,” the report said. Other countries like Turkey have different uses for stablecoins (the report found that Turkish users tend to use them to earn yield, followed closely by trading).

“I think there is indeed a crypto-dollarization event in Nigeria, from what I can tell, where people are actively moving away from the naira and moving towards the dollar via stablecoins. I think it’s happening. It’s the first real crypto-dollarization event,” Carter told me.

He, however, cautioned that it was not certain that one could “quantify that 15% of the devaluation (of the naira) is due to cryptocurrencies,” especially since the survey targeted cryptocurrency users. But the findings show that Nigeria may have reason to be concerned.

Aside from Nigeria, the study was able to show that stablecoins, when used by some in emerging markets, provide access to exposure to the US dollar, which could be interpreted as a boon for the US.

But, as noted above, there is currently no regulatory framework for stablecoin issuers, even though Circle – the company behind USDC – is looking to go public. But Carter also believes that issuers are “stuck” because none of them can issue interest-bearing stablecoins.

“All interest-bearing stablecoins are issued offshore,” he said. Carter cited the example of Paxos, which has an interest-bearing stablecoin in Dubai despite being a U.S.-based company. Mountain Protocol and Ethena’s offerings are also offshore.

“I think interest-bearing stablecoins are going to displace regular stablecoins at the margin over time. So they can’t do that in the United States because the Securities and Exchange Commission is so adamant about making it a security, right? So that’s one of the issues that has… stymied us at the moment,” Carter explained.

The report highlights that there is no single answer to why stablecoins are so heavily dollarized.

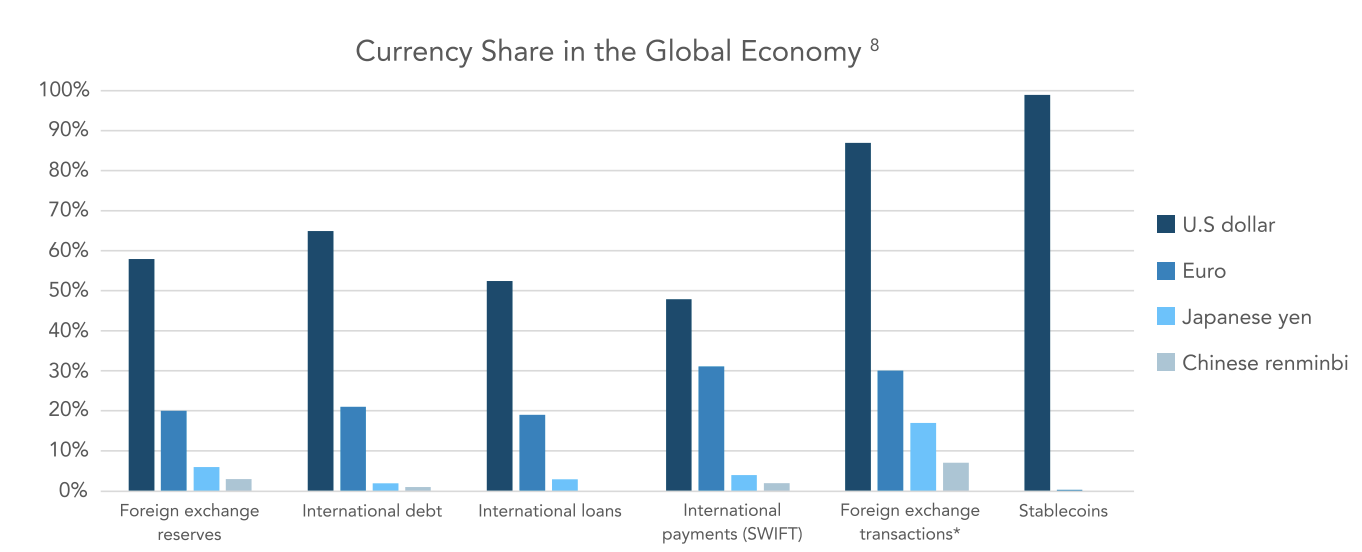

“The US dollar is the world’s reserve currency, but in no other category of use does it dominate to the same extent as stablecoins,” he stressed.

But there is no denying that stablecoins seem to have achieved their goal. Time will tell whether the United States will take advantage of this.

An edited version of this article first appeared in the Empire Daily Newsletter. Subscribe here to not miss tomorrow’s edition.

Start your day with the best cryptocurrency news from David Canellis and Katherine Ross. Subscribe to the Empire newsletter.

Explore the growing intersection of crypto, macroeconomics, politics, and finance with Ben Strack, Casey Wagner, and Felix Jauvin. Subscribe to the On the Margin newsletter.

The Lightspeed Newsletter is the latest Solana news delivered to your inbox every day. Subscribe to daily Solana news from Jack Kubinec and Jeff Albus.