Ethereum’s fall to its lowest level in more than a year is testing Wall Street trading that has taken the token deeper into institutional portfolios.

Data from CryptoSlate shows the second-largest cryptocurrency fell to $1,506 in the past 24 hours, its lowest level since April 2025, extending a broad crypto selloff that has already drained leverage from derivatives markets and pushed traders into defensive positioning.

Importantly, the decline is not limited to the ETH spot market, as the digital asset is also seeing a broader deterioration in regulated ETF flows, centralized exchange deposits, and derivatives positioning.

This comes at a time when overall crypto market sentiment has weakened significantly, with Bitcoin falling to a four-month low near $60,000, while Ethereum has erased much of its market support.

ETF Outflows Weaken Ethereum Institutional Supply

The pressure has been most visible in the ETF market, where products that gave institutions a regulated way to buy Ethereum have become a source of persistent outflows.

Data from SoSoValue shows that spot ETH ETFs have recorded four straight weeks of withdrawals totaling over $870 million.

During this period, the funds recorded a 17-day outflow streak broken by a single day of inflows, when investors added $19.3 million.

As a result, sosoValue data shows that the total assets of spot Ethereum ETFs declined by more than 70%, from their peak of $30 billion to $8.71 billion, which equates to approximately 4.01% of Ethereum’s circulating market capitalization.

This reversal weakened one of the main arguments behind Ethereum’s institutional expansion. ETFs were expected to expand access to the asset, increase liquidity, and provide traditional investors with a cleaner way to gain exposure without directly manipulating tokens.

However, this demand has subsided as the price of ETH has fallen and investors have reduced risk on digital assets.

FX Flows Add Another Supply Risk

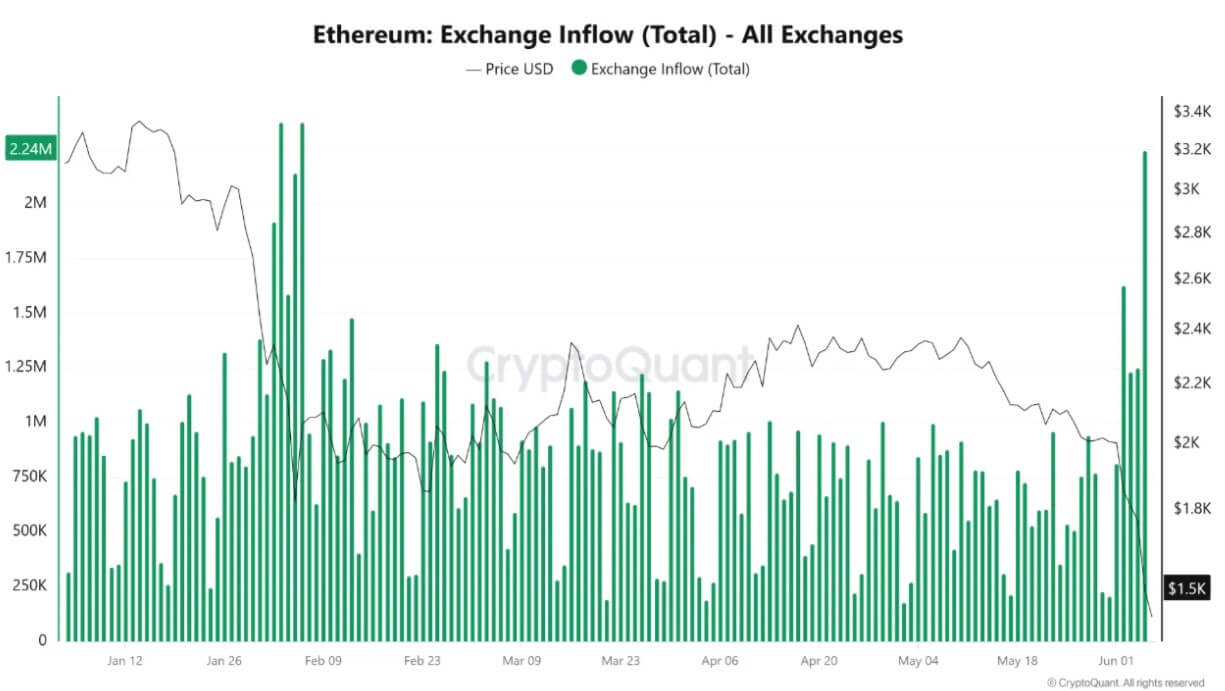

As institutional forces of demand weakened, the physical supply available on liquid trading platforms experienced a sudden and substantial expansion.

CryptoQuant data shows that Ethereum flows to trading platforms surged to around 2.24 million ETH in a single day, the highest level in four months. Binance accounted for over 1.16 million ETH of these flows, more than half of the total.

This increase in active supply is visible in the high-profile on-chain movements that constitute stark evidence of liquidity migration.

Notably, a wallet linked to Ethereum co-founder Joseph Lubin awoke after more than three years of dormancy, mobilizing 80,001 ETH, valued at approximately $122 million.

This massive shift embodies the broader trend of long-dormant capital moving out of cold storage to seek active trading platforms and liquid architectures amid growing market tension.

Large inflows to trading platforms do not automatically mean investors are selling. They may reflect market making activity, collateral movements, internal transfers or portfolio restructuring in times of stress.

However, traders monitor these metrics closely because coins held on exchanges are easier to sell or use in derivatives activities than coins placed in private wallets.

The timing made this increase harder to ignore. Ethereum was already trading near $1,580 when inflows accelerated, while Bitcoin had fallen to $59,000. This combination suggested that investors were moving their assets during a market-wide reset rather than during a typical period of repositioning.

If foreign exchange deposits remain high, the market could face additional volatility in the short term.

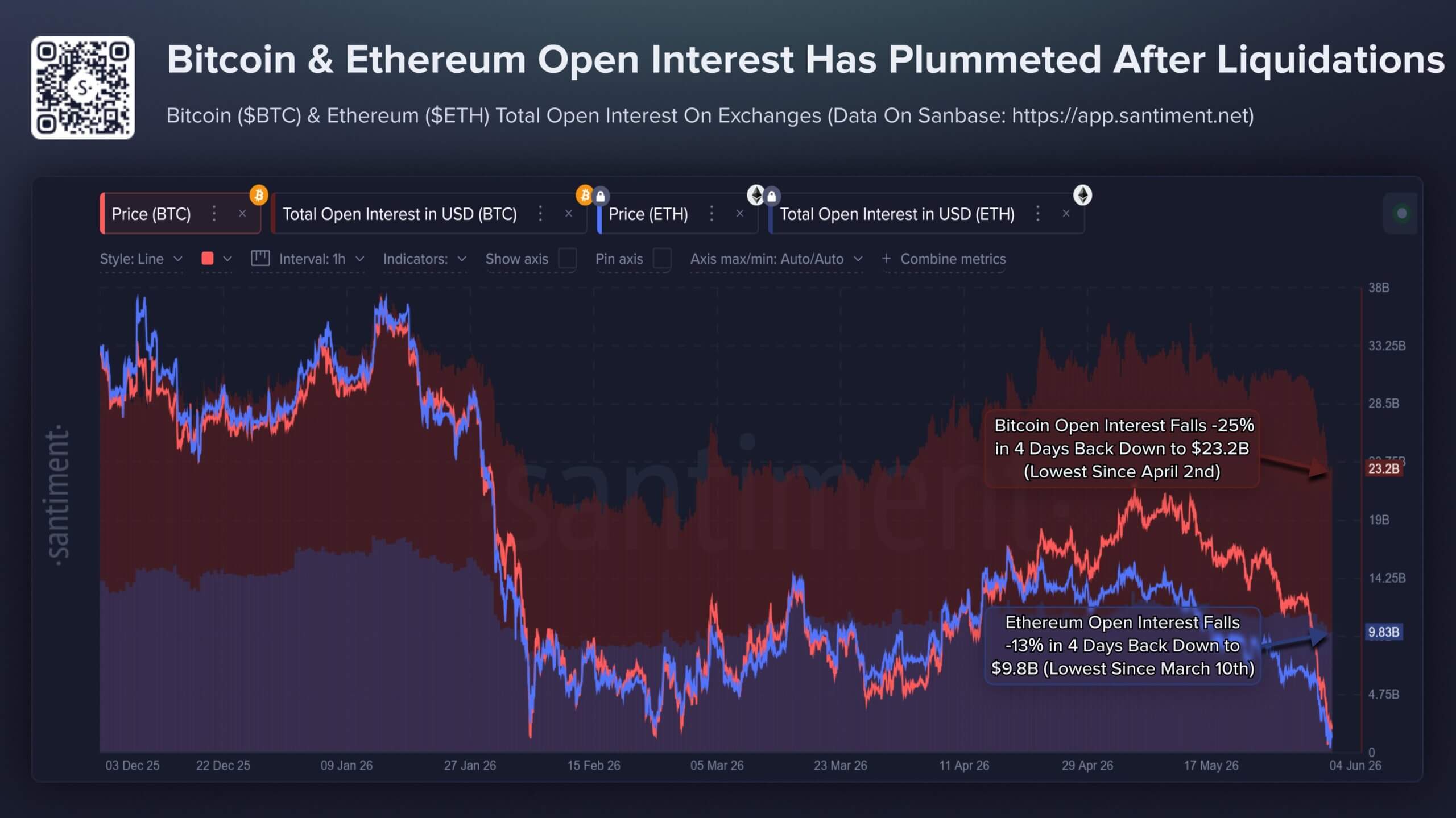

The deleveraging of derivatives deprives the capital market of rebound

The speed of the crypto market’s current decline has been accelerated by a massive deleveraging cycle on leveraged futures platforms.

As spot valuations rapidly deteriorated, automated liquidation engines on major exchanges systematically closed underwater long positions to protect the integrity of the clearinghouse, thereby amplifying organic selling pressure.

Data analyzed by Santiment shows that this wave of liquidation effectively wiped out a massive block of hot money over a narrow four-day window:

- Total Bitcoin Open Interest: Contracted by around 25%, falling to $23.2 billion, marking its lowest operating aggregate since early April.

- Ethereum Total Open Interest: decrease of 13%, reaching $9.8 billion, a structural low not seen since March.

Although this aggressive deleveraging leaves the underlying market structurally healthier by eliminating speculative excesses and overextended margins, it introduces an immediate liquidity void.

The sharp decline in open positions demonstrates that the speculative floor has thinned, leaving the market highly vulnerable to further spot pressures due to the lack of immediate leveraged capital available to initiate a classic V-shaped recovery.

As a result, retail sentiment has reached its most pessimistic level since mid-February.

The company noted that social metrics reveal an exponential increase in capitulation phraseology, with organic social discussions increasingly associating terms like “Bitcoin” and “altcoins” with terminal descriptors like “dead,” “finished,” “done,” and “ending.”

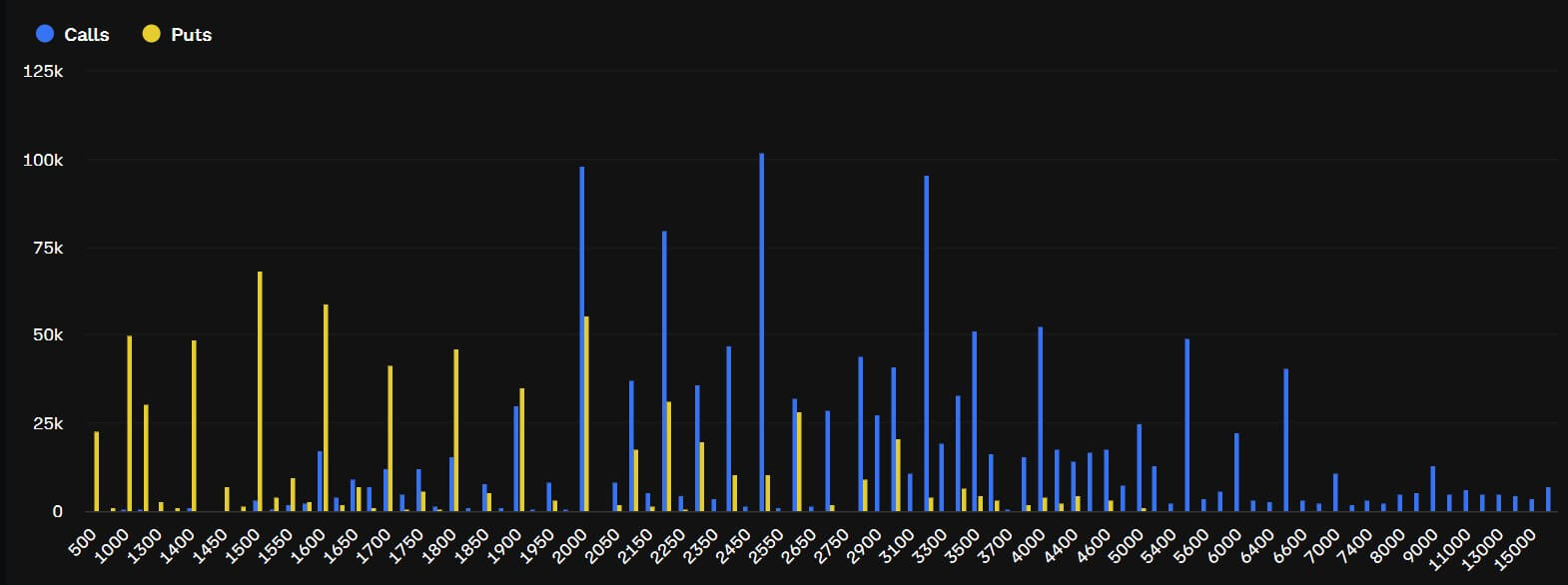

Traders are hedging for a break below $1,500

The buildup of stress on ETFs, exchange flows, cost bases and leveraged markets has focused attention on the ETH options market, where traders are paying more to protect against further decline.

Data from Deribit shows that demand for downside protection has increased sharply. The put-to-call premium for ETH options increased 3.7x on Friday and has shown consistent excess demand for put options since Monday. Put contracts give their holders the right to sell at a fixed price, making them a common hedge when traders expect further losses or want to protect against a disorderly move.

ETH open interest has clustered around several dips. Traders built about $108 million in open interest around the $1,500 strike, while the $1,400 strike attracted about $75 million. The $1,000 strike generated approximately $78 million in investment.

These levels do not mean that the market expects ETH to fall to $1,000 immediately. Instead, they show traders paying to protect themselves after multiple support signals weaken at the same time.

Data from BlockScholes shows that the change has also occurred in volatility prices. ETH’s short-term implied volatility has increased from a year-to-date low of 36% to 67%, signaling that traders now expect larger price swings in the near term.

This move was accompanied by a greater bias towards out-of-the-money put options. The seven-day ETH options bias has increased to around -14%, from around -3% to -4% in late May. Additionally, put demand also extended across maturities of 7, 14, 30 and 90 days.

This broadening shows that traders are not just covering a single event or short-term movement. They are bracing for the possibility that Ethereum’s weakness could expand if ETF outflows continue, exchange inflows remain elevated, and large holders remain below key cost levels.

The next test is whether $1,500 becomes a floor or a trigger. A stabilization of ETF flows and a decline in foreign exchange deposits could help ease the pressure.

Without it, the options market’s emphasis on downward moves could become the clearest signal of where traders expect the next round of selling to be focused.