In some of today’s craziest Bitcoin news, the “never sell” doctrine that Michael Saylor built into the strategy’s (MSTR) structural DNA is now being nuanced by the company that invented it, and the revision exposes a tension that has been building among Bitcoin cash traders since the 2022 bear market: ideological commitment to perpetual accumulation ultimately meets the arithmetic of fiduciary duty.

During Strategy’s Q1 2026 earnings call, Chairman and CEO Phong Le explicitly stated that the company would consider selling Bitcoin to buy US dollars or pay down debt if it was accretive to Bitcoin per share, a direct break from the passive accumulation posture that has defined the model since August 2020.

Genius Group has completed a complete liquidation of Bitcoin under debt pressure. Nakamoto Holdings sold around $20 million worth of BTC at a realized loss of around 40%. The doctrine encounters counterexamples observable on a large scale.

BREAKING: Michael Saylor Says Strategy Could Sell Bitcoin to Fund Dividends “Just to Send the Message”

He says he wants to ‘rip your wings’ from short sellers betting $MSTR must sell shares to finance dividends. pic.twitter.com/jUCiG6bwM3

– Crypto India (@CryptooIndia) May 6, 2026

The structural importance is not that the strategy sold Bitcoin; this has not yet been done in the new framework. What is important is that the board-level framework has shifted from accumulation as the end goal to Bitcoin per share as the guiding metric. This distinction has complex implications for every corporate treasury operator who has modeled their approach on Saylor’s original model.

DISCOVER: Best Crypto to Buy Right Now – Updated Guide from CoinSpeaker

Bitcoin News Today: The architecture of capital behind the doctrine – and why it only works on one scale

The mechanism works as follows: The strategy funds Bitcoin purchases not through operating cash flow, but through the continuous issuance of new shares through market programs and convertible notes sold to institutional buyers who accept below-market yields in exchange for exposure to Bitcoin upside via the MSTR equity premium.

The flywheel remains active as long as the stock is trading at a significant premium to NAV, because this premium allows the company to issue shares at prices that are dilutive in terms of number of shares but accretive in Bitcoin per share – each new dollar raised buys more Bitcoin than the proportional dilution costs existing holders in BTC-denominated terms.

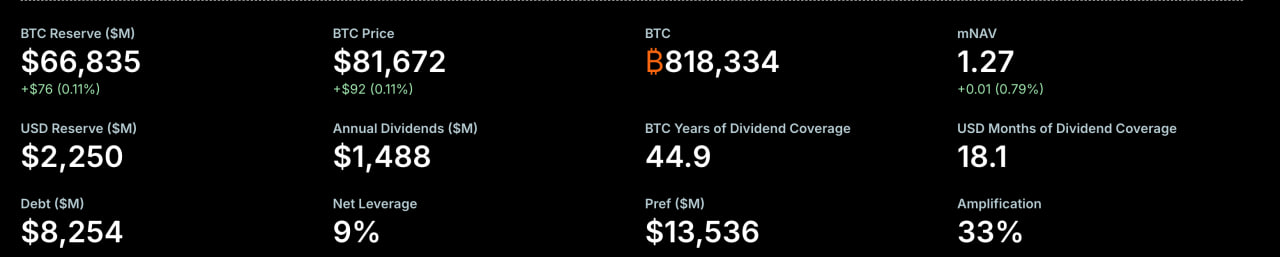

Strategy held 818,334 BTC at the end of Q1 2026, acquired at a total cost of $61.81 billion and an average price of approximately $75,500 per coin, or nearly 4% of Bitcoin’s total supply.

Source: Strategy

Its dollar reserve stood at $2.25 billion as of December 2025, established specifically to service preferred dividends and debt without requiring Bitcoin sales. The company reported a BTC return of around 9% year-to-date, measuring Bitcoin’s growth per share rather than price appreciation. It is not a measure of feeling. This is an engineering output.

The problem for smaller operators is that this architecture requires a persistent mNAV premium, an institutional appetite for convertible paper, and a balance sheet large enough to absorb mark-to-market losses without triggering covenant violations.

Strategy recorded a net loss of $12.5 billion in the first quarter of 2026 due to the decline in the price of Bitcoin and absorbed it. Most corporate treasuries cannot absorb such an order of magnitude.

EXPLORE: Best Ethereum Wallets for 2026 – Updated Guide from CoinSpeaker

following

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article is intended to provide accurate and current information, but should not be considered financial or investment advice. Because market conditions can change quickly, we encourage you to verify the information for yourself and consult a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. Hailing from crypto since 2017, Daniel leverages his experience in on-chain analytics to write evidence-based reports and in-depth guides. He holds certifications from the Blockchain Council and is dedicated to providing “insight gain” that overcomes market hype to find real utility for blockchain.