Bitmine plans to slow its Ethereum purchases as its holdings approach 5% of the cryptocurrency’s supply, ending a year of rapid accumulation that made the company the network’s largest holder of enterprise tokens.

In his July message to the president, Thomas Lee said Bitmine had accumulated 5.7 million ETH, or about 4.8% of the supply, but would gradually approach the 5% threshold rather than continuing to buy at its previous pace.

This change opens a new phase for Bitmine. The company plans to direct more capital toward investments in staking, Ethereum infrastructure, and financial services, as it seeks to expand the economic use of the network and bolster the value of tokens already on its balance sheet.

A self-imposed ceiling emerges

Bitmine’s decision to stop at nearly 5% reflects the complications that arise when a public company becomes one of the largest staking owners and operators on a proof-of-stake network.

Lee linked the move in part to changes at the Ethereum Foundation, the nonprofit that has long supported blockchain development. He said discussions with people connected to the foundation persuaded Bitmine to avoid accelerating purchases during the transition.

Lee said:

“At the moment, I think we should not try to accelerate and have more focus beyond 5%.”

This restriction introduces a consideration largely absent from corporate Bitcoin treasury strategies. Ethereum holders can stake their tokens, operate validators, and collect rewards for helping secure the network, giving a large treasury an operational role beyond holding the asset as a reserve.

Owning 5% of ETH would not give Bitmine control of Ethereum. His total holdings also differ in the amount he has committed to invest and the share of validators he operates.

The position nevertheless gives Bitmine significant staking capacity. The company leveraged this opportunity through MAVAN, its Made in America validation network, which Bitmine describes as the largest institutional Ethereum staking platform in the world.

Notably, Bitmine reported $45.7 million in staking and validation revenue for the quarter ended May 31, following the launch of native staking last November. This figure included $3.5 million related to the acquisition of staking operator Pier Two.

The strategy leaves Bitmine heavily exposed to ETH price movements.

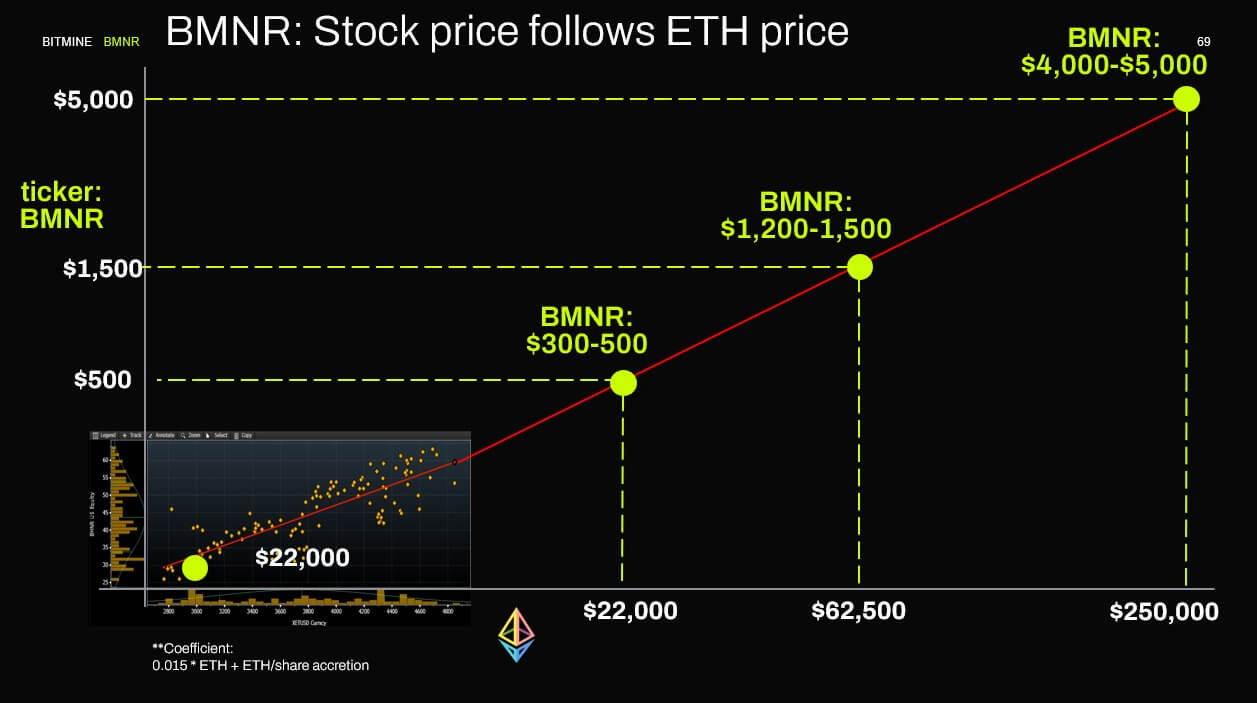

Lee said the correlation between the company’s stock and Ethereum is about 90%, indicating that investors continue to treat the stock largely as a proxy for cryptocurrency despite its growing staking and investment operations.

The goal approach therefore creates a strategic challenge. Continuing to accumulate at its previous pace could increase concentration issues, while slowing purchases removes the primary mechanism Bitmine previously used to increase exposure.

The company now needs to generate more value from the ETH it already owns.

Bitmine expands further into the Ethereum ecosystem

As direct accumulation slows, Bitmine plans to deploy more capital into the Ethereum ecosystem and businesses, which could increase demand for the network.

Lee said the company was the largest investor in ETH Labs, Ethereum Institutional and ETH Systems. The organizations are working on areas such as institutional adoption and confidential infrastructure for companies that want to conduct financial activities on Ethereum.

Bitmine also plans to fund additional Ethereum organizations, business partners, and public goods as the Ethereum Foundation reduces its role in certain areas.

The strategy directly serves Bitmine’s financial interests. Greater adoption of Ethereum could strengthen demand for ETH, increasing the value of its 5.7 million token reserve and supporting its stock price.

Its investments could also give Bitmine a larger role in determining which infrastructure projects and institutional products receive commercial support.

However, Lee characterized this position as neutral, as the company could potentially become a permanent asset, since Bitmine does not sell products to the institutions it hopes to attract.

Additionally, the company’s mandate now extends beyond native Ethereum projects. Lee said Bitmine would also consider investing in traditional crypto and financial services companies that could transfer securities, payments, funds and other assets on blockchain networks.

This is a broader strategy than the initial focus on accumulating ETH and building staking infrastructure. Lee argued that the distinction between crypto companies and conventional financial institutions will become less relevant as both begin to use the same settlement systems.

According to this thesis, a brokerage, custodian, or asset manager moving its operations onto Ethereum-based rails could contribute to network adoption as directly as a crypto protocol.

Lee said:

“We simply want to strengthen the Ethereum ecosystem, which in turn contributes to the price of Bitmine.”

At the same time, Bitmine is also developing capital market products to finance these expansion efforts. The company recently launched a 9.5% perpetual preferred security under the symbol BMNP, which Lee compared to STRC, one of Strategy’s preferred stock instruments.

BMNP was issued at $80 in June and had risen to around $86 at the time of its presentation. The stock gives investors a yield-bearing claim on a company whose balance sheet remains dominated by Ethereum while providing Bitmine with another source of funding alongside common stock issuance and staking revenue.

The proceeds could support investments in Ethereum infrastructure and financial services, allowing Bitmine to increase its exposure to the ecosystem without purchasing ETH at its previous pace.

Bitmine’s entry into the New York Stock Exchange and inclusion in the Russell 1000 could also expand its investor base. Membership in an index can generate demand for funds that track the benchmark and make the company more relevant to active managers who use it to evaluate performance. The Russell 1000 represents approximately 1,000 of the largest companies in the U.S. stock market.

However, the new capital comes with additional obligations. Cumulative BMNP dividends continue to accumulate even during market downturns, as falling ETH prices reduce the value of Bitmine’s reserves.

This increases pressure on Bitmine to convert its staking operations and ecosystem investments into sustainable returns.

Tokenized Finance and AI Underpin Lee’s Most Optimistic ETH Scenario

Bitmine’s broader strategy ultimately rests on Lee’s belief that tokenized finance and autonomous AI agents could transform ETH into working capital for institutions and software.

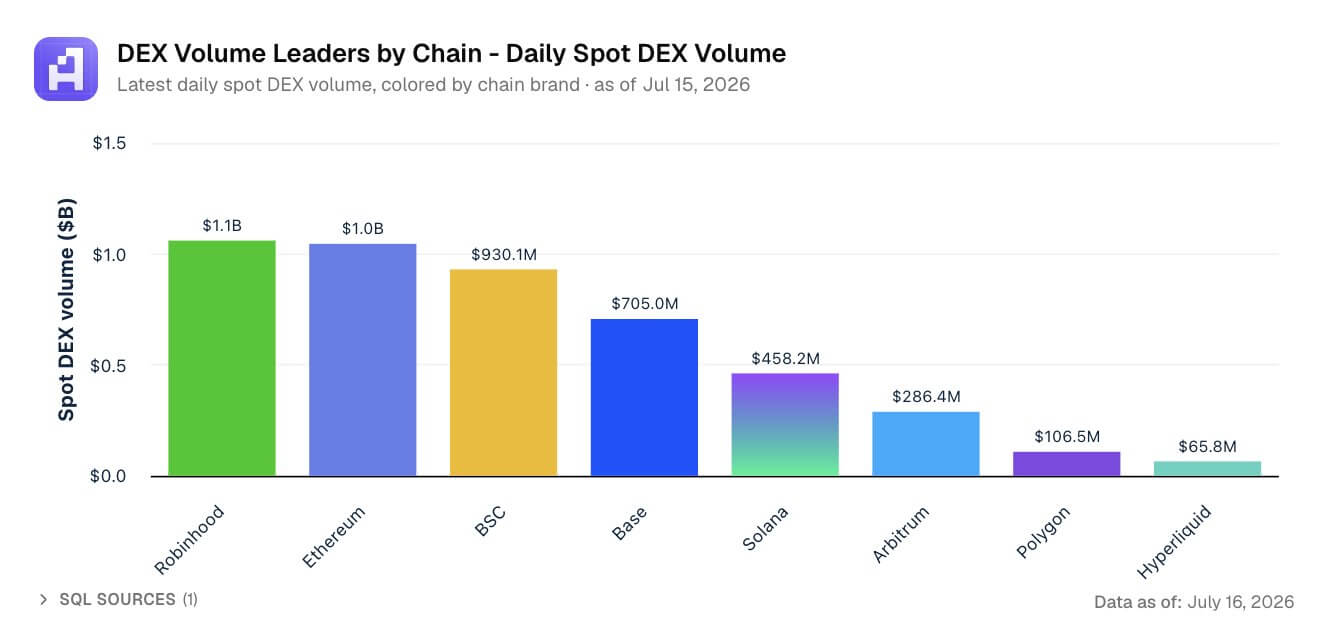

Robinhood Chain offered its clearest example. The Ethereum Layer 2 network uses ETH as its native gas token and is designed to support tokenized stocks, exchange-traded funds, private assets, and other financial instruments. Lee said his transactions were ultimately settled on the Ethereum mainnet.

Since its launch, the network has seen significant success, with its daily decentralized spot trading volume surpassing that of Ethereum over the past 24 hours.

For Lee, this activity shows how brokerages could move stocks, funds, and other traditional assets onto blockchain infrastructure while creating recurring demand for ETH.

He also cited tokenization projects involving BlackRock and JPMorgan as evidence that financial institutions are moving toward blockchain-based issuance and settlement.

However, the relationship is not automatic. Layer 2 networks can process substantial activity while paying relatively low fees to Ethereum, while users can transact through stablecoins without directly holding ETH.

Lee’s thesis assumes that institutions will still need significant ETH balances as working capital once tokenized markets reach sufficient scale.

Artificial intelligence could add a second source of demand. Lee expects autonomous agents to earn revenue, execute transactions, manage accounts, and purchase services without ongoing human direction.

These agents would need payment networks that operate 24 hours a day and programmable rules limiting how assets can be used.

Smart contracts could provide these controls by restricting an agent’s authority and recording what they own, spend or transfer. Ethereum could capture some of this machine economy if agents and their operators need ETH to execute and settle transactions.

Tokenized finance and AI therefore play complementary roles in Lee’s argument. Financial institutions could bring large pools of assets onto Ethereum-linked networks, while autonomous agents could create a new population of users transacting at machine speed.

Together, they support his description of ETH as “productive money,” an asset held because institutions and software need it to function, rather than just because investors expect its price to rise.

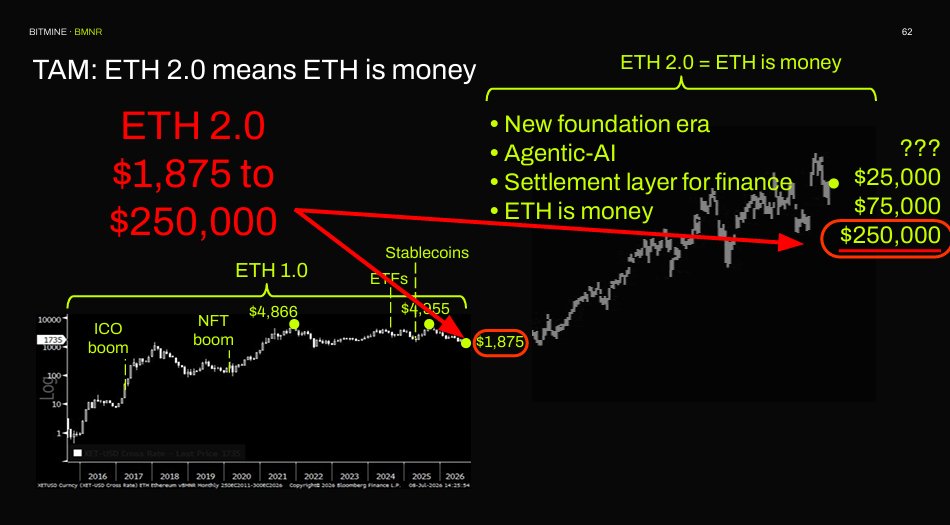

This projected demand also supports the more aggressive valuations discussed in the presentation. Lee discussed $25,000 and $75,000 scenarios before citing a $250,000 estimate put forward by Ethereum co-founder Joseph Lubin and Etherealize.

Although he did not adopt the higher figure as a formal target, Lee argued that ETH could see radical upside potential if Ethereum becomes a major financial settlement and automated trading platform.

To achieve this valuation, Ethereum would need to capture a significant share of both markets while competing with rival blockchains, stablecoins, private ledgers and bank-controlled payment systems.

This would also require increased network usage to translate into sustained demand for ETH rather than allowing applications to minify or abstract the token entirely.