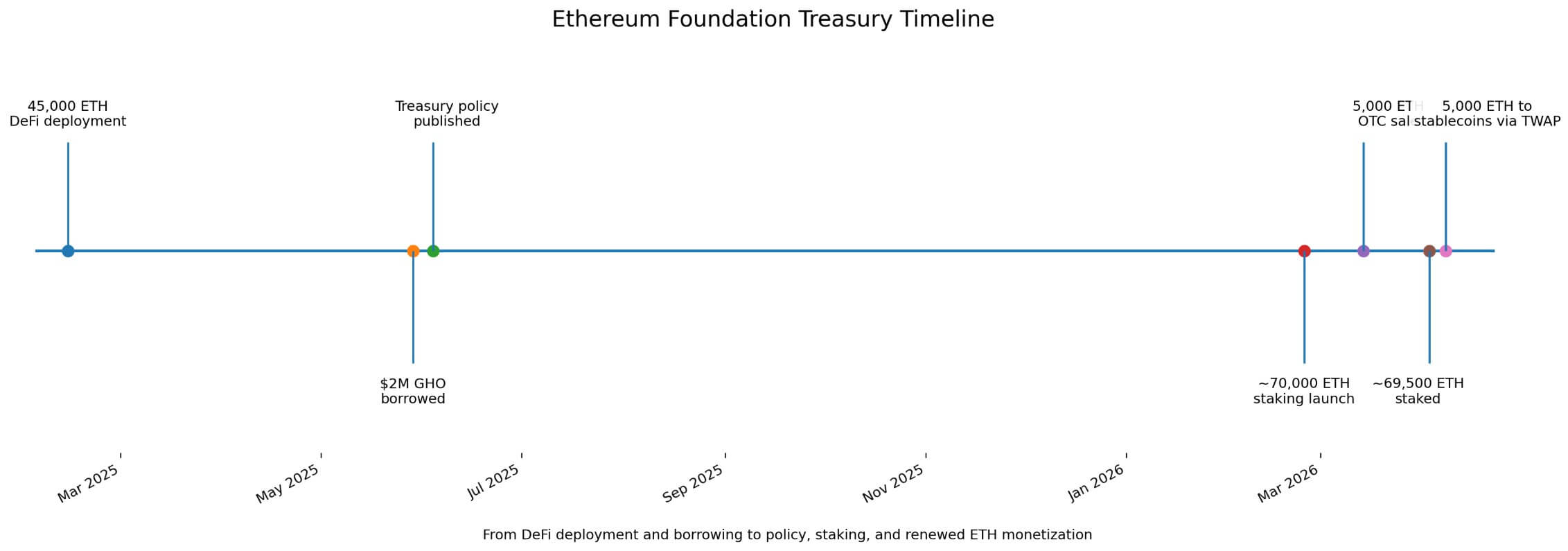

The Ethereum Foundation (EF) announced on April 8 that it will convert 5,000 ETH into stablecoins via CoWSwap’s TWAP feature to fund research, grants, and donations.

The announcement reopened a debate about what the foundation’s treasury overhaul was supposed to accomplish. Over the last year, EF moved treasury assets to DeFi, borrowed against ETH collateral, and then launched a staking initiative centered on around 70,000 ETH.

The reality outlined in EF’s June 2025 Treasury Policy suggested a different model. It tied monetization to a fiat currency-denominated operational buffer and kept ETH sales, staking, and stablecoin borrowings within the same treasury framework.

On February 13, 2025, EF Treasury announced that it had deployed 45,000 ETH on Spark, Aave Prime, Aave Core and Compound. On May 29, she borrowed $2 million in GHO against her Aave position.

This move carried symbolic weight as it showed that EF was using DeFi rails to raise working capital without selling ETH for spot.

By early April, this interpretation had seeped into retail discourse, as a Reddit post claimed that EF was “no longer selling.” One commenter responded that “it’s good they stopped selling.”

Despite anecdotal evidence, this kind of chatter shows how the strongest version of the thesis had already entered circulation before EF announced the conversion on April 8.

The sale continues

When EF launched its staking initiative on February 24, it announced that it would stake 70,000 ETH, with the rewards going back to the treasury.

On March 14, he completed an OTC sale of 5,000 ETH to BitMine at an average price of $2,042.96. On April 3, on-chain activity pushed the total staked to around 69,500 ETH, close to the target. Then came the April 8 CoWSwap conversion, highlighting that selling and staking had already been operating side by side for weeks.

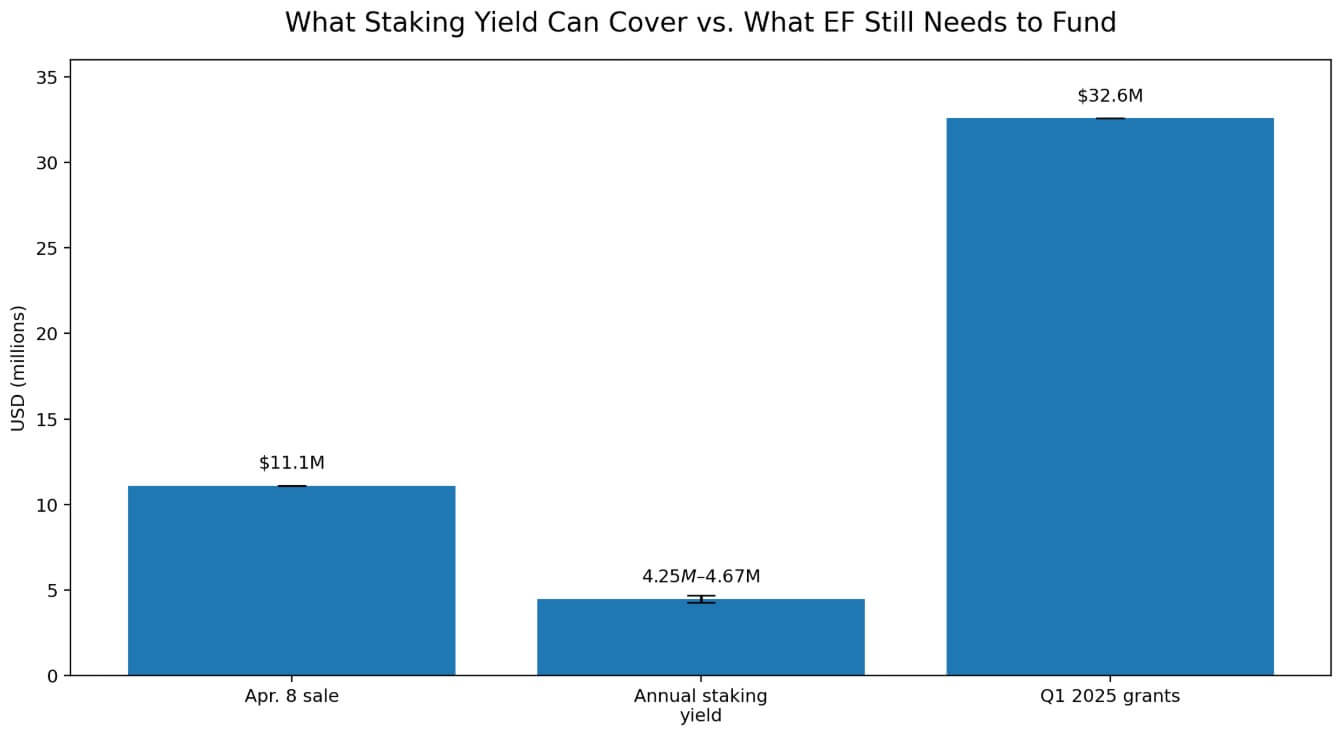

At an ETH price of around $2,220.76, a conversion of 5,000 ETH equates to around $11.1 million, while benchmark ETH staking rates in early April were between 2.73% and 3.00%.

Applied to 70,000 ETH, this produces approximately 1,912 to 2,102 ETH per year, worth approximately $4.25 to $4.67 million at current prices. A single sale of 5,000 ETH equates to approximately 2.4-2.6 times the annual yield of the entire 70,000 ETH staking round.

The staking program improves cash efficiency and reduces funding requirements, but it remains well short of the scale needed to replace cash sales.

The June 2025 EF framework set annual operating expenses at 15% of cash and the operating cushion at 2.5 years, implying a fiat currency reserve equal to 37.5% of cash.

Applied only for illustration purposes to EF’s latest comprehensive cash overview, the October 31, 2024 report showed $970.2 million in total cash and $181.5 million in non-crypto assets, implying a target policy reserve of approximately $363.8 million.

EF had already publicly added stablecoin exposure after this snapshot, deploying 2,400 ETH and approximately $6 million worth of stablecoins into Morpho in October 2025, and subsequently announced additional ETH to stablecoin conversions in October 2025 and April 2026.

The exact current size of EF’s fiat bucket and whether tokenized RWA holdings have already been added in hardware size are still unknown. The 2024 snapshot should therefore be treated as an illustration rather than a substitute for the current assessment.

EF’s own allocation update showed $32.6 million in grants for the first quarter of 2025. At the current price of ETH, this equates to approximately 14,700 ETH. The April 8 conversion covers only about 33% of this quarter’s total grants, excluding protocol research, personnel, operations and broader industry support.

Yielding and borrowing leaves the fiat currency budget intact and still requires periodic monetization.

Potential results

EF’s bullish argument relies on simple Treasury arithmetic, as a higher ETH price and lower long-term operating ratio would allow the foundation to maintain its dollar reserve while monetizing fewer coins.

| Scenario | What changes | Probable cash flow effect |

|---|---|---|

| Bull case | ETH Price Rises, Long-Term Operating Ratio Declines | Fewer coins need to be sold to maintain the fiat buffer |

| Reference case | The mixed strategy continues | Staking, DeFi, borrowing and periodic sales coexist |

| Bear case | ETH Price Weakens, Spending Pressure Increases | More ETH may need to be monetized to preserve the trail |

| Key consequence | Reserve target remains denominated in fiat currency | The “less selling” talk collapses if ETH falls |

In this context, staking rewards and selective borrowing can reduce quarterly sales and give EF more flexibility in choosing venue, whether through OTC blocks, TWAP execution, or conservative DeFi positions.

Treasury modernization would then manifest itself in lower cadence, smaller clips and better execution.

The downside scenario follows the same framework in reverse, since EF’s reserve target is worded in fiduciary terms.

A lower ETH price may force greater monetization to preserve runway, especially if the foundation builds on its countercyclical mandate and spends more aggressively in tougher market conditions.

In this setup, a large staking sleeve still generates yield, but reserve requirements may increase faster than that yield offsets.

Public expectations based on “less sales” then clash with the balance sheet discipline that EF had already included in its policy.

The conversion of April 8 brought this discipline back into the spotlight. EF’s treasury strategy had already combined DeFi deployment, stablecoin borrowing, staking, and periodic ETH sales.

The market narrative extended beyond the written policy and beyond the foundation’s own post-staking transaction history.