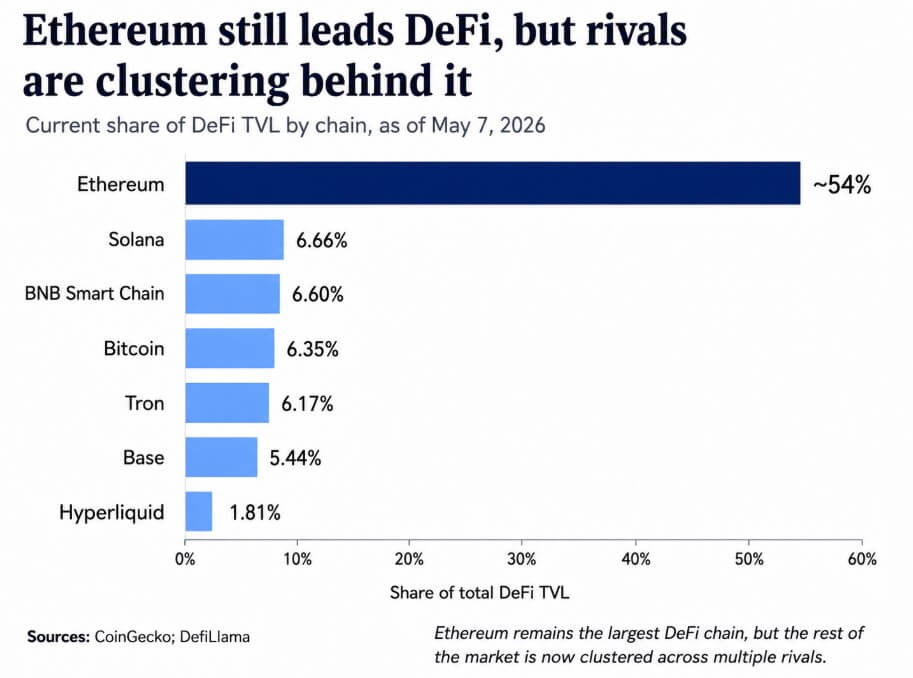

Ethereum’s share of total value locked (TVL) in DeFi fell from 63.5% at the start of 2025 to around 54% as of May 7, near the lowest level recorded since May 2025.

DefiLlama estimates Ethereum’s current TVL at $45.4 billion, while the stake-absorbing chains each have a distinct function, such as decentralized exchange (DEX) flow, stablecoin settlement, BTC collateralization, consumer onboarding, and perpetual trading.

Solana owns 6.66% of DeFi TVL, BNB Chain 6.60%, Bitcoin 6.35%, Tron 6.17%, Base 5.44% and Hyperliquid 1.81%. This consolidation defines that DeFi has moved from a single Ethereum-centric hub to a network of specialized rails.

Which channels have conquered the market

BSC has built its position on distribution linked to Binance. In Q2 2025, CoinGecko reported that PancakeSwap volume jumped 539.2% quarter-over-quarter to $392.6 billion, accounting for 45% of the top 10 DEX volume, with Binance Alpha routing transactions directly through PancakeSwap.

DefiLlama currently shows BSC with $5.55 billion in TVL and $739.6 million in 24-hour DEX volume. Binance has deepened this integration through Alpha Earn, which allows users to provide liquidity to PancakeSwap V3 directly from Binance Wallet, and Alpha 2.0 integrates DEX trading into the Binance Exchange interface.

Binance controls the front end, PancakeSwap executes the transaction, and BSC collects the volume.

Tron operates on a different axis. DefiLlama shows $89.6 billion in stablecoins on Tron, with USDT accounting for 97.86% of that figure, while 24-hour DEX volume stands at just $55.5 million.

Tron’s DeFi TVL, worth $5.19 billion, underplays its role as the chain with the largest stablecoin flows in crypto, functioning as a dollar settlement rail with low application diversity and huge throughput.

Bitcoin’s DeFi TVL reached $5.34 billion, with a dominance of 6.35%, up 13.4% over 30 days, despite a 24-hour DEX volume of just $338,516. The difference defines the BTCFi thesis is that capital migrates to Bitcoin to generate yield and guarantee.

Bitcoin’s DeFi role emerges as a productivity layer, where capital is earned through collateral and lending protocols.

The base is the most important part of the competitive map as it operates inside the Ethereum stack while eroding Ethereum’s overall L1 share. Coinbase built Base as an Ethereum layer 2 (L2) on top of the OP stack, and the distribution advantage is that Base App works in over 140 countries.

DefiLlama shows $4.58 billion in Base TVL, $4.93 billion in stablecoins, and $854.97 million in 24-hour DEX volume.

Activity that migrates from Ethereum L1 through Base continues to settle into the Ethereum security model. Coinbase has consolidated Ethereum block space behind its own consumer distribution layer and routes this activity through an execution environment operated by Coinbase.

Hyperliquidity demonstrates that liquidity can now be organized entirely around execution quality. DefiLlama shows $1.52 billion in TVL on Hyperliquid L1, along with $9.37 billion in 24-hour perpetual volume, $42.4 billion in 7-day, and $8.94 billion in open interest.

Hyperliquid runs fully on-chain perpetual and spot order books on a purpose-built chain, and these volume numbers confirm that perpetuals have grown large enough to form a standalone DeFi liquidity hub.

Open interest and daily turnover measure Hyperliquide’s true market weight, as TVL only captures a fraction of the channel’s activity.

Solana operates at a scale that puts it in a separate category from specialty rails. CoinGecko shows $15.26 billion in 24-hour on-chain trading volume on Solana, the largest of any chain, and DefiLlama estimates its DeFi dominance at 6.66%.

Solana functions as a general-purpose high-throughput trading platform, simultaneously distributing flows across DEXs, memecoins, liquid staking, and institutional tokenization efforts. Its continued scale confirms that the DeFi market supports both specialized rails and large-scale competitors.

| Chain | Main role in DeFi | TVL | Key activity indicator | Why it grew |

|---|---|---|---|---|

| BNB Smart Chain | DEX feed linked to Binance | $5.55 billion | $739.6 million in 24-hour DEX volume | Binance distribution, PancakeSwap routing |

| Tron | Stablecoin settlement rail | $5.19 billion | $89.6 billion in stablecoins, 97.86% USDT share | Dollar transfers, reduced diversity of applications |

| Bitcoin | BTC/BTCFi Guarantee | $5.34 billion | $338,516 in 24-hour DEX volume | Productive BTC, collateral utility |

| Base | Ethereum L2 linked to Coinbase | $4.58 billion | 24-hour DEX volume of $854.97 million, stablecoins of $4.93 billion | Consumer Onboarding, Coinbase Distribution |

| Hyperliquid | Perpetual place | $1.52 billion | $9.37 billion in 24-hour person volume, $8.94 billion in OI | Quality of execution, dedicated market |

| Solana | General Purpose Trading Platform | 6.66% share | On-chain trading volume of $15.26 billion over 24 hours | Wide range of high throughput applications |

What Ethereum still controls

Ethereum’s absolute position is still strong. DefiLlama shows $45.4 billion in TVL, $165.5 billion in stablecoins, $1.45 billion in 24-hour DEX volume, and $1.61 billion in 24-hour perps volume.

Ethereum is home to the premier lending protocols, deepest stablecoin liquidity pools, and institutional integrations that most DeFi infrastructure relies on as a safety net.

The 30-day TVL data adds important context: Ethereum is up 13.9% over this period, alongside Bitcoin at 13.4%, Base at 10.5%, Hyperliquid at 7.3%, Tron at 6.8% and BSC at 2.9%.

The market is developing simultaneously on several chains and the redistribution of shares reflects the specialization during this expansion.

Any analysis of dominance based solely on TVL requires a methodological caveat. DefiLlama counts the TVL chain as the sum of the TVL protocol and by default excludes liquid staking from the chain totals.

Price appreciation can move TVL numbers without net capital inflows, and DefiLlama tracks connect TVL separately. A complete picture requires stable coin supply, transaction counts, and transaction volumes alongside TVL, each telling a different story about where DeFi activity is actually concentrated.

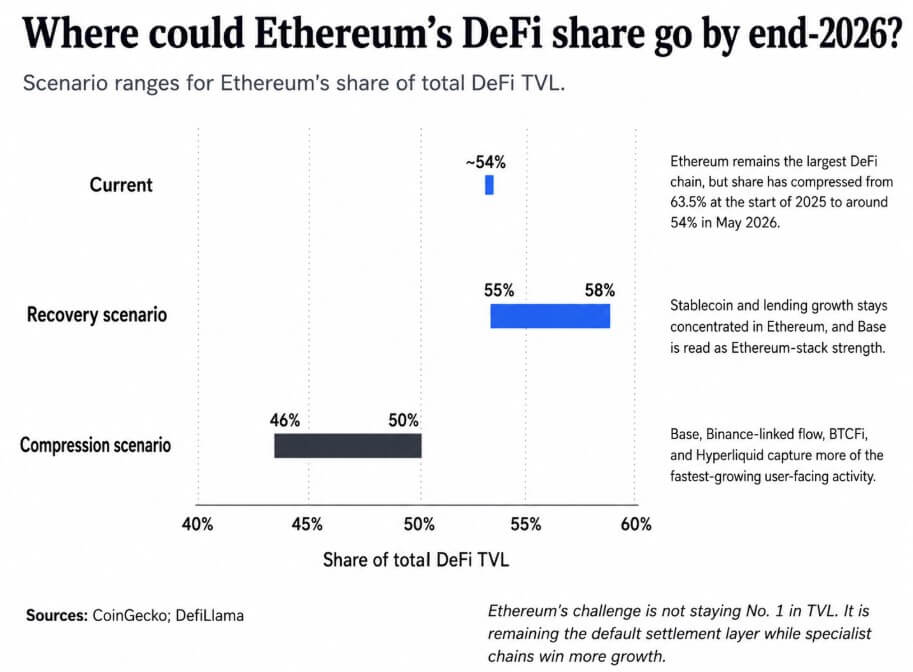

Two paths for Ethereum’s share

If stablecoin and lending activity grows faster than specialized sites, and if Base’s growth is interpreted in the market as the strength of the Ethereum stack, Ethereum’s TVL share could rebound towards 55% to 58% by the end of 2026.

Ethereum’s $165.5 billion stable base and depth in top-tier lending protocols provide the foundation for this path.

If Binance deepens Alpha integration, Coinbase continues to push Base through its consumer apps layer, BTCFi collateral usage expands further, and Hyperliquid maintains its grip on on-chain perpetuals, Ethereum’s share compresses to 46%-50%.

In this scenario, Ethereum functions as the primary settlement and custody layer of DeFi, while most user-facing activity flows through specialized venues with better distribution economies.

The real challenge for Ethereum is maintaining the settlement layer while specialized chains capture the use cases with the fastest user growth.

TVL’s absolute lead is large enough to absorb compression, and the coin’s stability and institutional depth strengthen its position as DeFi’s core balance sheet.