Bitmine has invested more than $10 billion in ETH, making it the largest Ethereum treasury company and a yield-generating bet on the network’s proof-of-stake economy.

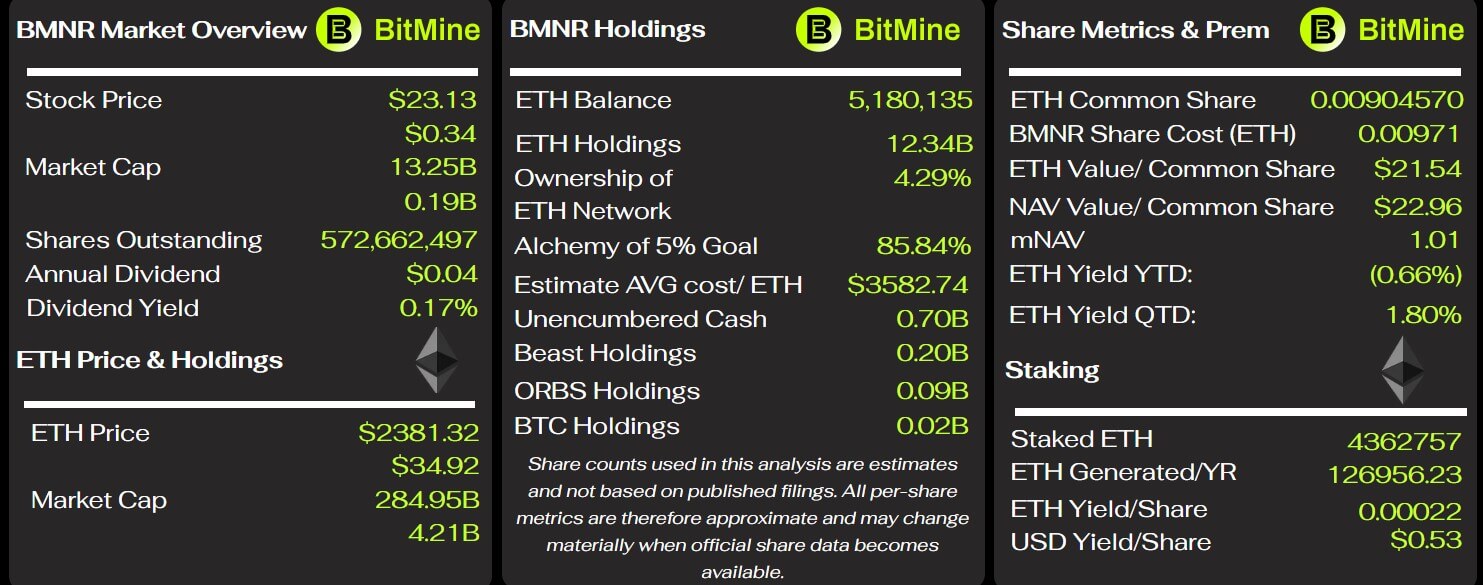

On May 4, the Las Vegas-based company said its ETH position stood at 4.36 million tokens, valued at $10.2 billion at the average ETH price of $2,336.

This position represents over 84% of BitMine’s total ETH holdings and gives the company one of the largest visible enterprise exposures to Ethereum’s validation system.

BitMine reported holding 5.18 million ETH as of May 3, approximately 4.29% of Ethereum’s total supply. The company also reported 200 Bitcoin, $700 million in cash, an investment in Beast Industries, and a stake in Eightco Holdings, bringing total crypto, cash, and moonshot holdings to $13.1 billion.

Ethereum Treasury Bet Becomes a Staking Deal

BitMine said its staking operations generate annualized revenue of approximately $297 million, based on a seven-day annualized yield of 2.91%.

President Thomas “Tom” Lee said projected annual rewards could reach $352 million once the company’s ETH holdings are fully staked through MAVAN, its Made in America validation network, and other staking partners.

The disclosure moves BitMine’s Ethereum strategy from a balance sheet accumulation move to a test of recurring revenue.

Public companies have used Bitcoin primarily as a Treasury reserve asset, with Michael Saylor’s strategy defining the corporate accumulation model. Ethereum gives BitMine a different structure because the asset can be staked directly into the network to earn protocol rewards.

BitMine’s scale makes it a public market proxy for Ethereum’s staking economy. Investors in its BMNR stock are no longer only exposed to variations in the market price of ETH. They are also exposed to the company’s ability to manage validator infrastructure, earn network rewards, and grow its position on Ethereum over time.

Notably, BMNR traded an average daily volume of $625 million over five days as of May 1, ranking 173rd among U.S.-listed stocks.

This liquidity gives the company a public capital channel through which investors can express their views on accumulating and staking Ethereum without directly owning the token.

Ethereum Validator Queue Shows Wider Demand

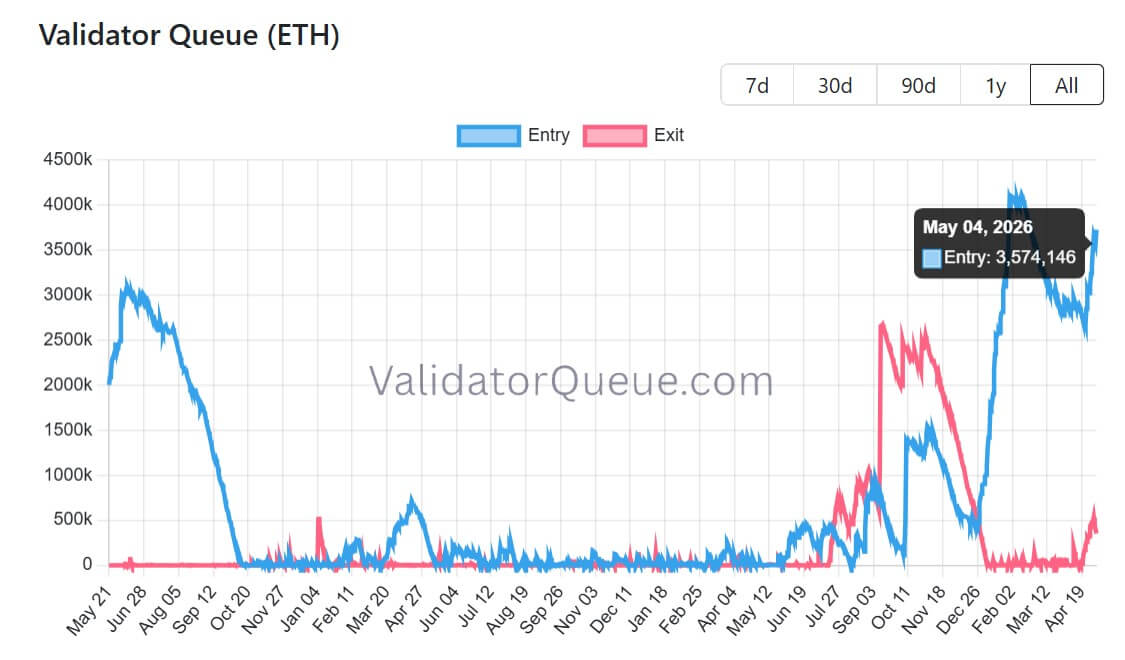

BitMine’s staking push comes as Ethereum’s validator input queue has increased sharply, signaling renewed demand for ETH as a yield-generating asset, even as the token’s price narrative remains contested.

Data from ValidatorQueue showed approximately 3.72 million ETH waiting to enter the validator set, with an estimated activation time of over 64 days. Around 346,000 Ethereum was waiting to be released, with an estimated wait of around six days.

The network had approximately 898,000 active validators, 38.6 million ETH staked, and a stake rate of approximately 31.7% of supply.

Ethereum limits the amount of ETH that can enter or exit validation at a time through a churn mechanism designed to protect consensus stability. This limitation can create a long queue when new deposits exceed the rate at which validators can be activated.

Meanwhile, the queue doesn’t mean all that ETH is already earning rewards. The deposited Ethereum must wait for activation before starting to participate in validation.

Nonetheless, the imbalance between entry and exit queues shows that more capital is trying to enter Ethereum staking rather than exiting it.

This is a notable signal for the Ethereum markets. A larger staking base can immediately reduce the liquidity supply, while validator rewards turn ETH into a productive asset for holders willing to accept lock-in, technical, and operational risks.

Return comes with operational risk

Ethereum staking differs from crypto lending because the rewards come from the protocol rather than the borrower.

Validators lock ETH as collateral, run software, attest to blocks, and help secure the network. They earn rewards when functioning correctly and can lose rewards if they go offline. In more serious cases, validators may be penalized with outages for harmful behavior.

While this structure has made staking attractive to institutions seeking native crypto yield, it also creates a new category of operational risk for public companies.

Indeed, an ETH holding company staking at scale must manage validator availability, client selection, custody, key management, and exposure to staking partners.

For BitMine, the revenue opportunity is clear. A 2.91% annualized return on billions of dollars of Ethereum creates a significant revenue stream. However, the risk is that staking is not passive, unlike holding spot Ether in a corporate wallet.

The company’s MAVAN infrastructure is at the heart of this strategy. If BitMine continues to stake most of its Ethereum, its cashflow model will depend not only on the price of ETH, but also on the performance of the validator and the reliability with which staking rewards can be generated over market cycles.

This makes BitMine’s model different from a conventional crypto treasury company. It seeks to hold ETH, earn the digital asset, and potentially increase its share of the asset over time through protocol rewards.

Ownership is not the same as control

Additionally, BitMine’s huge ETH holdings also raise a more specific question about the decentralization of the blockchain network.

Under Ethereum’s proof-of-stake system, validators integrate Ethereum into the network and participate in consensus.

Ethereum.org states that an attacker with more than 33% staked Ether can interfere with the purpose, while higher thresholds present greater risks. Finality depends on a qualified majority of two-thirds of the Ether votes staked at checkpoints.

This means that BitMine’s 4.29% share of the total ETH supply is economically significant but does not, in itself, grant control of Ethereum.

Given this, the more relevant question is how much of the active ETH stake BitMine controls, whether the stake is split between operators and clients, and how much of the network becomes dependent on a small group of institutional validators.

The Ethereum decentralization debate has long focused on staking concentration, liquid staking protocols, centralized exchanges, and client diversity. Large pools and staking providers can influence the network as they operate validators, shape defaults, and coordinate around upgrades.

The emergence of BitMine adds a new corporate layer to this debate. A public company that invests billions of dollars in Ethereum can strengthen the security of ETH by increasing the value locked in validation.

However, it may also intensify concerns if an increasing share of validator power is concentrated within a limited set of software operators, custodians or customers.

Public Markets Test Ethereum Staking Economy

The market question is whether BitMine’s strategy will be treated as a leveraged ETH trade, a staking revenue vehicle, or a hybrid of the two.

If Ethereum increases, the company’s cash value increases. If staking returns remain stable, BitMine can generate recurring rewards denominated in ETH. If the validator queue remains high, the company’s initial stake scale could become more valuable as new entrants must wait longer to earn rewards.

At the same time, the opposing risks are also evident. The decline in the price of ETH can quickly reduce the monetary value of the Treasury.

Staking returns may drop as more Ethereum enters the validation process. Operational errors, partner concentration or customer failures can turn a profitable strategy into a source of losses.

For Ethereum, BitMine’s decision shows how proof-of-stake has changed the asset’s role in public markets. ETH is no longer held solely as a speculative token or reserve asset.

At BitMine’s scale, it is also used as productive capital capable of generating revenue, securing the network, and reshaping the debate over institutional participation.