In the latest Bitcoin news, Strategy (MSTR) is trading about 43% below what a discounted cash flow (DCF) model says it’s worth, and it just sold $216 million in Bitcoin to pay preferred dividends. These two facts are in direct tension, and the resolution of this tension is what determines whether MSTR is a bargain or a value trap dressed up in attractive numbers.

The central question this analysis raises: Does the apparent discount in Strategy’s stock analysis reflect a genuine misvaluation of its Bitcoin holdings, or is it fair compensation for the capital allocation risk that common shareholders now assume?

DISCOVER: The best Meme Coin ICOs to invest in 2026

Bitcoin News: What the DCF Model Really Says

A discounted cash flow, or DCF, model works by estimating the amount of cash a company will generate for shareholders over time, then reducing those future numbers to a present dollar value using a discount rate that reflects risk.

Think of it as a question: How much is a stream of future payments worth to you today, given that tomorrow’s money is worth less than today’s money?

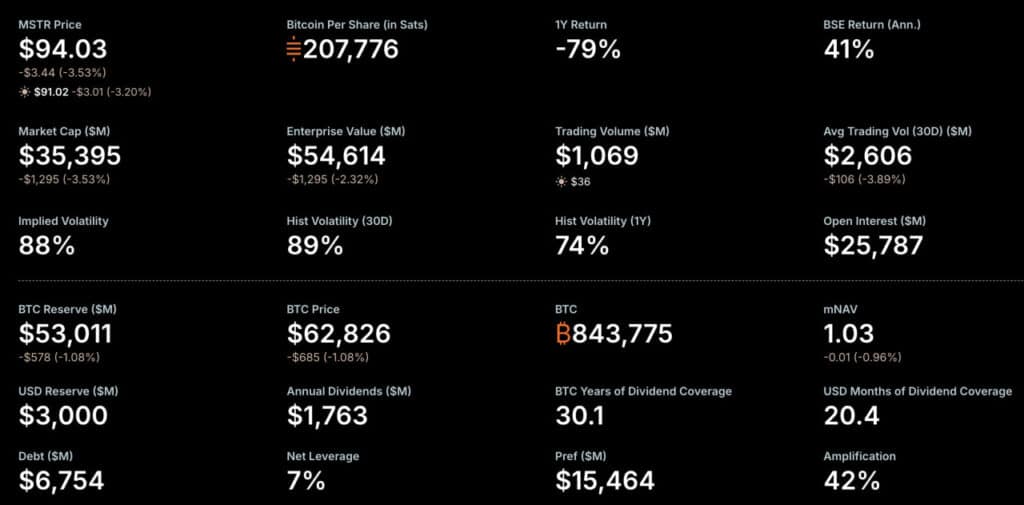

Analyst Bailey Pemberton of Simply Wall St applies this to the strategy and arrives at an intrinsic value of around $165 per share, placing this intrinsic value 43.1% above current stock price.

The model starts from a trailing twelve month free cash flow position of approximately $72 million in outflows and projects a recovery and growth trajectory from this negative base.

Simply Wall St gives Strategy a valuation rating of 4 out of 6 on its checklist, a mixed picture, not a screaming buy signal. Rising DCF and a price-to-book (P/B) ratio of 0.9x both indicate undervaluation, while the company’s concentrated exposure to Bitcoin and evolving cash flow mechanics pull in the other direction.

Looking at the P/B metric specifically, Strategy’s 0.9x compares to about 2.8x for the software industry as a whole and about 7.3x for its direct peer group as a whole, according to the same Simply Wall St analysis.

The market is pricing Strategy’s stock below the reported value of its net assets, which is unusual and generally signals either a troubled balance sheet or deep skepticism about asset quality.

DISCOVER: The Next 1000x Crypto Gem Ahead of Its Listing on Binance

The BTC monetization program is a game changer

For years, Strategy (MSTR) has built its identity as a pure Bitcoin accumulation vehicle, financing BTC purchases through the issuance of equity and debt without ever touching the underlying holdings. The BTC monetization program breaks this model.

Strategy recently completed a $216 million Bitcoin sale under this new program to fund preferred dividends on four preferred share classes: STRC, STRK, STRD, and STRF.

STRATEGY SOLD $216M worth of BITCOIN TO PAY DIVIDEND $MSTR NOW HOLDS $2.55B in Cash

– Bitcoin Archive (@BitcoinArchive) July 6, 2026

This is not a minor operational adjustment. This means that the company’s Bitcoin stack, the core asset that underpins every bullish valuation argument, is now a source of funding for financial obligations, not just long-term holding as the news claims.

This is extremely important for ordinary shareholders. When Strategy sells Bitcoin to fund dividend obligations, it increases concerns that capital allocation choices and Bitcoin price fluctuations could weigh heavily on the value of common stock.

The DCF model can incorporate a recovery in liquidity generation, but this recovery depends on Bitcoin performing well enough to more than offset the continued flight from preferred payments.

The program would also include broader capital allocation discretion than that exercised by Strategy.

EXCLUSIVE: Earn $10 USDC via Binance Signup

The post Bitcoin News: Strategy sold $216 million in BTC for dividends – Is the no-sell model officially dead? appeared first on 99Bitcoins.