- Stablecoins have become integrated into traditional finance, but many banks are mainly focused on the basic concept.

- You will find below some critical aspects of the stablecoins that banks must fully understand.

The Stablecoins, once a niche concept within the cryptocurrency ecosystem, have now positioned themselves as a critical actor in the global financial discourse.

In fact, some analysts argue that these stable tokens could emerge as a great competitor of the US dollar. According to Ambcrypto, two key factors support this hypothesis.

First, the growing adoption of stablescoins for cross -border transactions, in particular in the regulation of essential products such as crude oil and agricultural products.

Second, and above all, the growing international dynamics, in particular within the economies of the G20, for the development of a decentralized or non -USD alternative.

Consequently, the Stablecoins – notably the attachment (USDT) – have reached a market capitalization of 144.30 billion dollars, positioning itself as a leader in the evolving landscape of digital finances.

Understand stablecoins beyond speculation

For the context, Stablecoins are designed to maintain a 1: 1 ankle with assets like the US dollar. Unlike risk assets, stablecoins have a negative correlation with a wider market dynamic.

In simple terms, an increase in the domination of stables indicates a capital reallocation far from volatile assets, indicating a flight to liquidity. In this context, Stablecoins works as an instrument of disintegration.

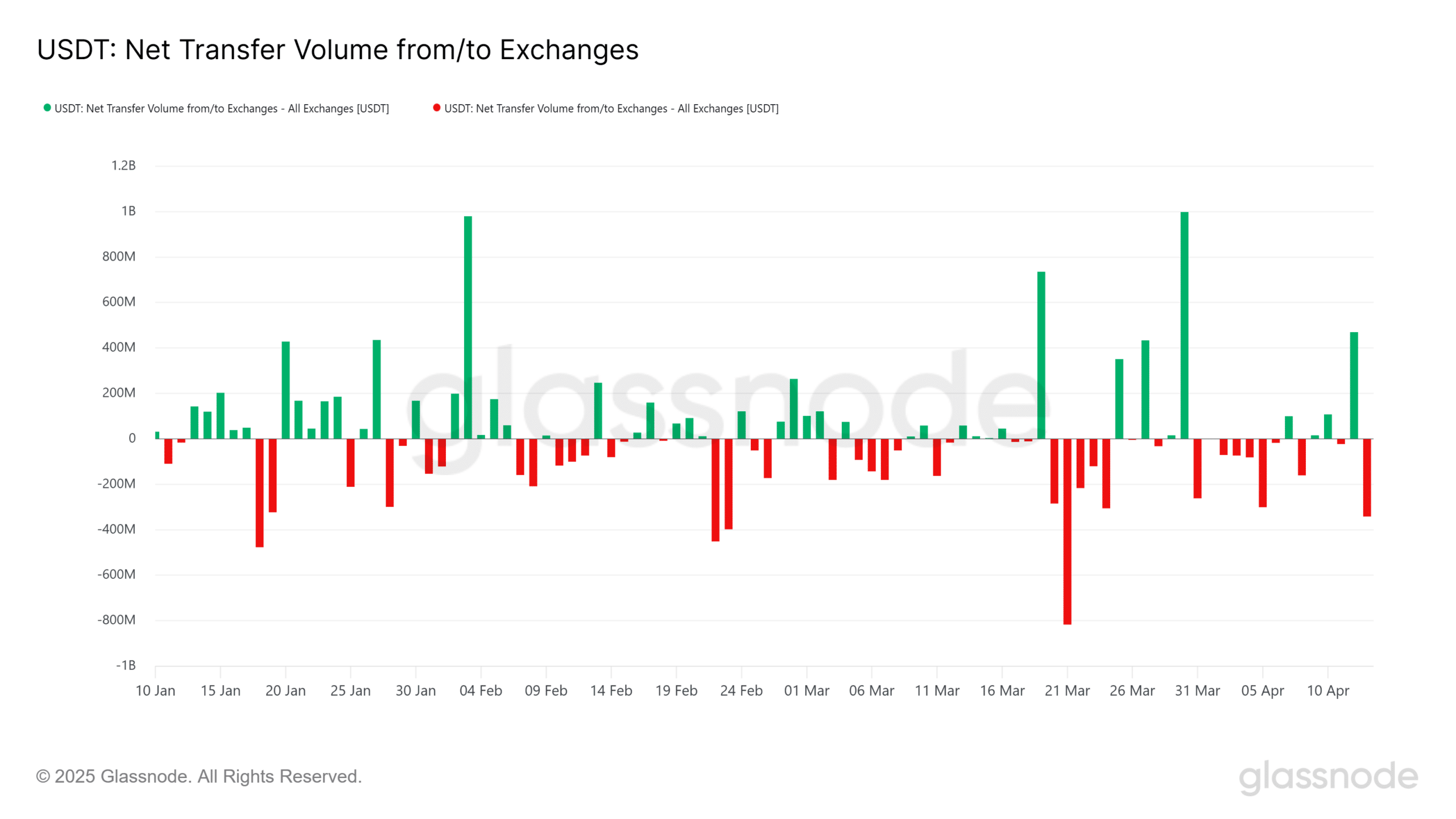

Illustrated, during the window from March 20 to 24, USDT Netflow Chart printed with pronounced red body candlesticks, reflecting high accumulation.

This coincided with the parabolic Bitcoin (BTC) movement to a local summit at $ 88,000, followed by a net corrective movement at $ 81,000.

Source: Glassnode

Consequently, their inherent stability makes them less speculative than other risk assets. However, many banks continue to misinterpret the strategic role of these stable tokens – often reducing them to simplistic Fiat proxies.

As the financial landscape evolves and decentralization gains structural relevance, below are certain key aspects of the stablescoins that banks should know.

Critical realities that banks must understand

Clear monitoring is essential for any asset class, but stablecoins are faced with a fragmented regulatory landscape.

For example, in the United States, the unclear competence between the dry and the CFTC creates confusion. The EU, on the other hand, evolves towards standardization with its mica frame.

Meanwhile, Asia has a mixed image. This global divergence complicates cross -border operations. In fact, while countries deploy their own digital currency pilots from the Central Bank (CBDC), Stablecoins can deal with stricter rules in the future.

But it doesn’t stop there. Even in fund transfer services, which require cross -border payments, banks must face regulatory obstacles to fully capitalize on this use case.

In conclusion, stablecoins offer significant use cases in the banking sector, improving transparency and decentralization.

However, for their potential to be fully achieved, banks must establish strict regulatory monitoring, rationalize cross -border payments and change their point of view – see stablecoins not as speculative competitors, but as the future of dominant funding.