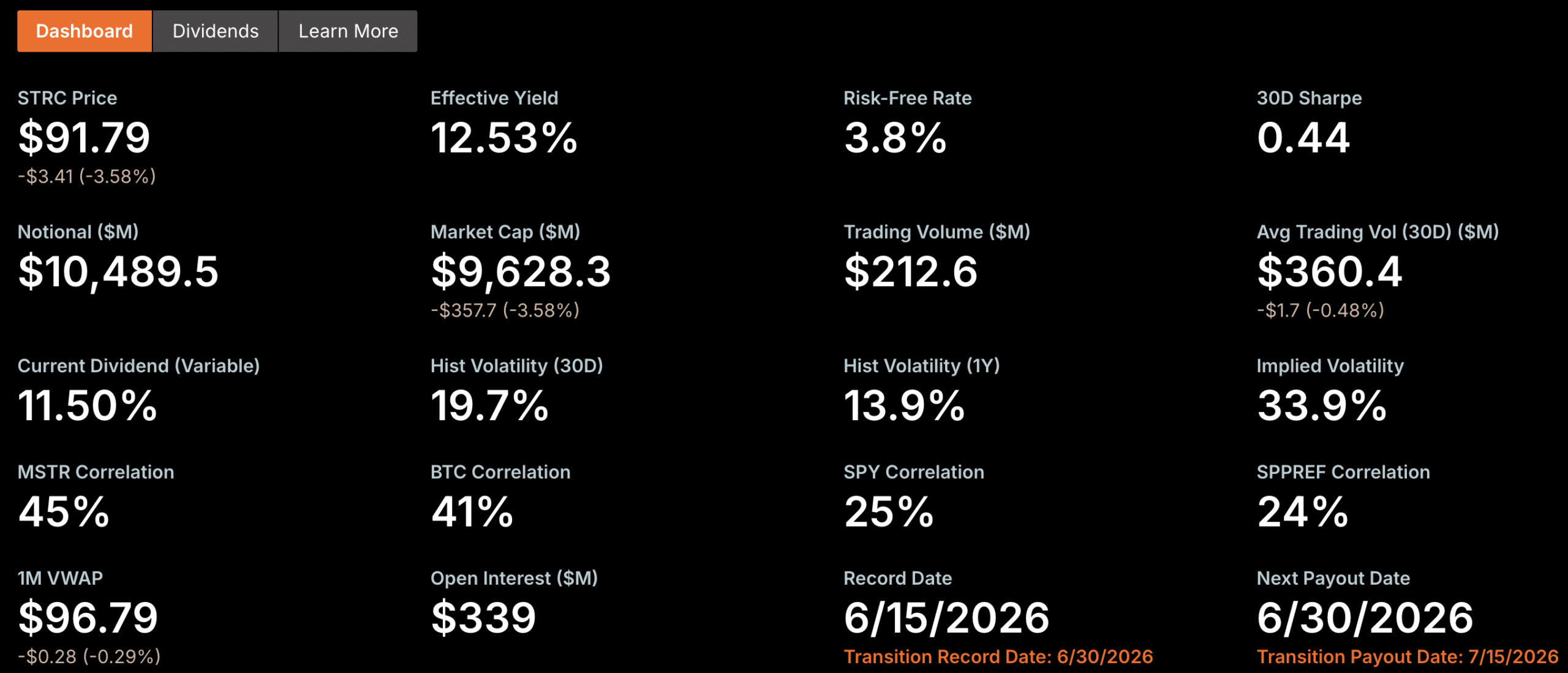

Saylor-led STRC perpetual preferred stock fell 3.58% to $91.79 on Tuesday, hitting a near-record low and sitting 8.2% below its $100 face value, and the reason matters beyond a bad session.

This drop signals a direct collision between Michael Saylor’s relentless Bitcoin cash accumulation plan and the cash obligations his company has incurred to preferred shareholders who have been promised a reliable 11.5% dividend.

STRATEGY’S “BITCOIN MACHINE” STRC STOCK SLIPS 8% BELOW PAR: WHAT DOES THIS MEAN AND HOW COULD IT RECOVER?

x– $STRC closed at $91.79 on June 16, down 3.58% for the day and about 8.2% below its par value of $100; although the company highlights an annualized growth of approximately 350% of the notional scale

– Gk (@gksolanky) June 17, 2026

The structural tension at the heart of this article is that every dollar the strategy deploys in BTC purchases is a dollar that is not in reserve to serve STRC’s dividend, and the market is now explicitly pricing in this conflict.

This drop in strategy data came as Bitcoin fell -2.5% overnight to just under $65,000, after climbing to $67,000 earlier this week before the retracement of the last 24 hours.

What is STRC and why Par level is important

$BTC failed to reclaim the $67,000-$68,000 zone.

Now the key level to maintain is $64,000-$65,000.

If Bitcoin loses this, it will eventually give back most of its short-term gains. pic.twitter.com/uI6P5k8oyD

— Ted (@TedPillows) June 17, 2026

STRC is Strategy’s variable-rate Series A perpetual expandable preferred stock, sometimes called “Stretch” – Saylor’s attempt to create a high-yielding, Bitcoin-adjacent fixed-income product. Think of it as a corporate bond with stock DNA: It pays a variable dividend designed to track around 11.5%, it has a target value of $100 per share, and it has no maturity date, which is what “perpetual” means.

The nominal $100 level is not just a psychological anchor. When STRC is trading at or above par, Strategy can issue new shares efficiently through at-the-market (ATM) programs, essentially selling preferred shares on the open market to raise new capital for Bitcoin purchases.

When it trades below par, this engine slows down. Selling new shares at $91.79 when the target price is $100 is like a company doing a deeply discounted rights issue: It works, but it dilutes the proposition for existing holders and signals market stress.

According to Cointelegraph, STRC is now below average since April 15, meaning this is not a single-day aberration. This is a one-month structural squeeze on Strategy’s preferred share funding mechanism.

DISCOVER: The best Meme Coin ICOs to invest in 2026

The dilemma between dividend strategy and accumulation strategy

(SOURCE: Strategy)

Saylor created a structural link with STRC, marketed as a “digital credit” alternative to money market funds, which offers a return backed by a large Bitcoin corporate stake.

The security of the dividend depends on the strategy maintaining cash reserves instead of continually purchasing BTC at high prices. STRC holders now view Bitcoin purchases as prioritizing accumulation over dividend security, even though the strategy reportedly has a 21-month cash flow and no margin call trigger.

Nick Ruck of LVRG Research notes that the broader sentiment of risk aversion in crypto has had an impact on investor interest. Despite a variable dividend yielding above 12%, continued selling pressure and concerns over Strategy’s growing capital structure are testing its stability.

With approximately $21 billion in debt securities, each new issuance of preferred stock complicates the capital structure, making it difficult for individual instruments to maintain their anchor price.

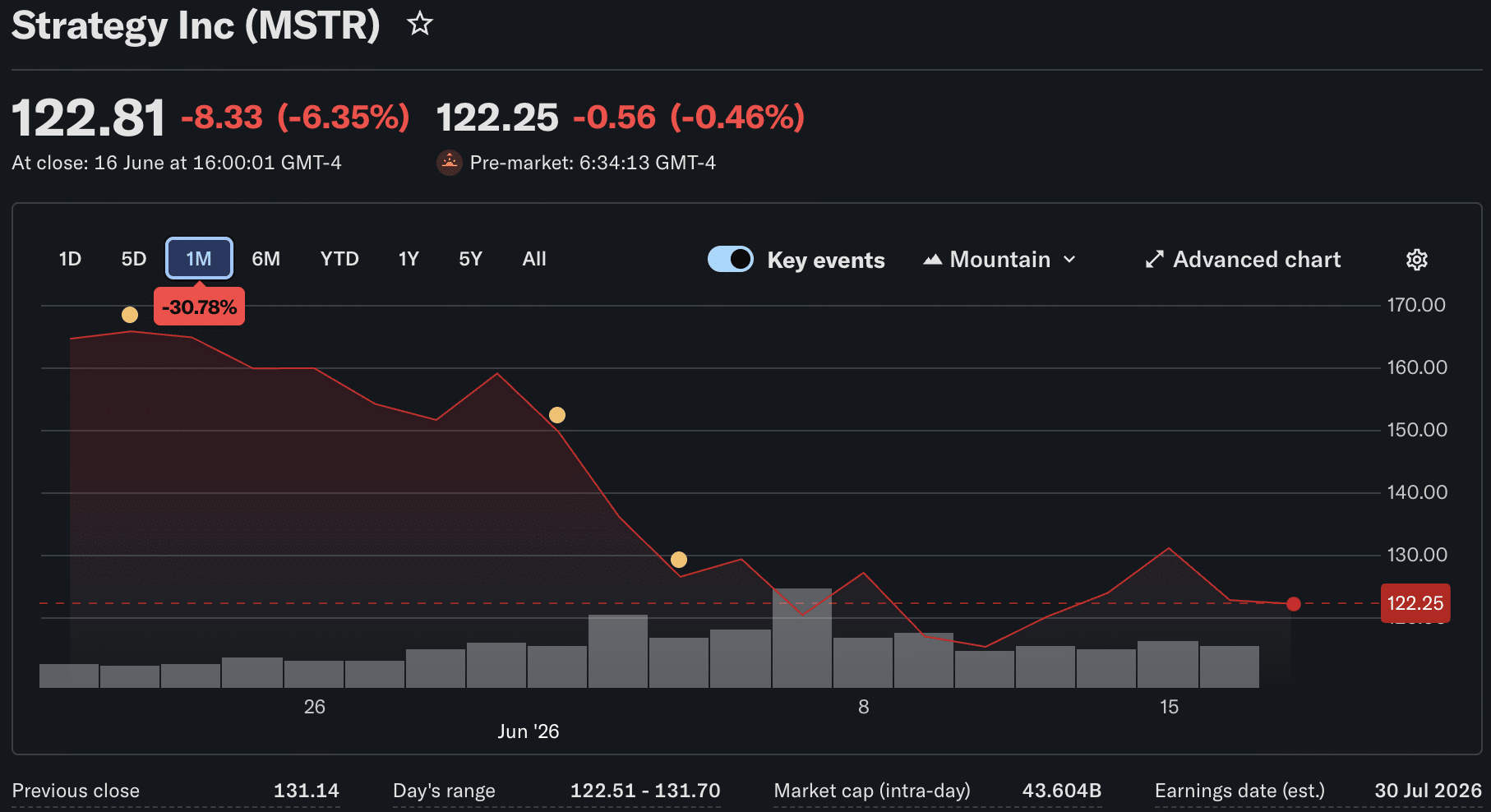

Strategy (MSTR) feels the same pressure

(SOURCE: Yahoo Finance)

MSTR shares saw a significant decline of 6.35% on Tuesday, closing at $122.81, marking a 67% decline over the past year. This glaring loss contrasts with Bitcoin’s performance, which did not fall as drastically.

The difference highlights the market’s revaluation of premium investors once paid for MSTR as a leveraged Bitcoin investment. At its peak in late 2024, MSTR traded at over 2.4 times its net asset value, but by January 2026, this premium had fallen to around 1.1 times.

In early June, MSTR made its first Bitcoin sale since 2022, selling 32 BTC for $2.5 million, which challenged the company’s previous narrative that it never sold. This sale, while modest relative to its total Bitcoin holdings, sent a strong psychological message: the company’s investment model may be conditional.

EXCLUSIVE: Earn $10 USDC via Binance Signup

SATA wins preferred stock comparison

The competitive pressure on STRC has a name: SATA. Strive’s floating rate perpetual preferred shares currently trade at exactly $100 – their face value – while offering an effective yield of approximately 13%.

This is a cleaner deal than STRC by almost every metric a fixed-income investor would apply: same instrument structure, higher yield, no discount to par, no overhang of a controversial Bitcoin accumulation strategy dominating overall risk.

When two similar products trade on the same market and one holds par value while the other trades at an 8.2% discount, the market expresses a clear preference.

STRC holders not only benefit from a lower price; they hold an instrument that signals financing stress while a competitor remains stable. This comparison is difficult to dismiss.

The broader landscape of Bitcoin-adjacent investment vehicles has also become more competitive. Yielding Bitcoin ETF structures and other institutional-grade products expand the menu of options for investors seeking crypto exposure with an income component, reducing the captive audience that STRC once enjoyed as a relative novelty.

EXPLORE: Best Crypto Presales with Asymmetric Upside Potential in Today’s Market

Strategy’s STRC Nears All-Time High as Bitcoin Buying Draws Fire appeared first on 99Bitcoins.